2026 Predictions: Enterprise AI

We're back with our annual predictions! Bigger and bolder than ever.

Happy 2026, everyone. January is always a magical time: new beginnings, ambitious OKRs — and sales reps “circling back” about software you’re still not going to buy. February always feels like a return to the grind: the start of ambitious new projects, the announcement of big funding rounds, and the thrill of back-to-back meetings.

(Note: Yes, this post is late - I’ve been heads down with deals. Sorry not sorry!)

Last year, I kicked off Scaling the Enterprise with a set of predictions on agents, data centers, and the products-vs-features reckoning in AI. Most of them aged well. This year, we move on to arguing whether foundation models will eat the application layer.

Here are my Top 10 predictions for Enterprise AI in 2026, written from the POV of someone who spends most of his time thinking: Will an enterprise actually adopt this?

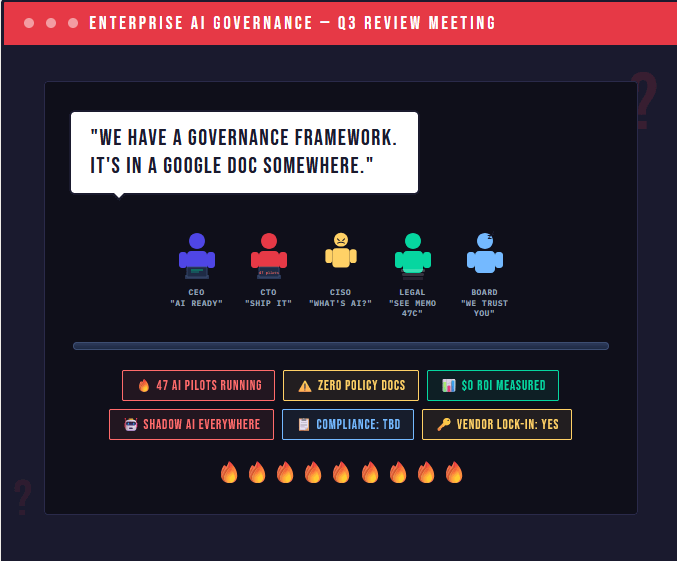

1. AI Governance Becomes a Competitive Advantage

Enterprise AI sprawl is real. Between copilots, agents, foundation models, internal fine-tunes, and third-party AI SaaS, most large enterprises now operate dozens of AI systems simultaneously. But how do you account for AI risk?

Winning organizations will build internal governance councils, cross-functional oversight, clear deployment playbooks, and defined risk thresholds. The enterprises that scale AI fastest will be the most focused and disciplined.

In 2026, I predict the AI Trust Layer becoming mandatory. A few companies I’m tracking in this space include Arize, Trustwise, Geordie AI, Reco AI, and Fiddler AI.

2. AI Might Take Your Job. But You’ll be Fine.

🔥 My spicy take is that AI’s impact on job destruction will be overblown. Yes, AI layoffs are coming. But society overall will benefit massively, and many new jobs will emerge for those willing to learn new, higher value skills.

Take yesterday’s announcement by Block about a 40% layoff of its workforce: while CEO Jack Dorsey was quick to blame AI for the cuts, the reality is that Block had become bloated and inefficient in recent years. The cuts were overdue (Wall Street responded with a 20% stock jump).

A report from McKinsey found that one-third of the jobs we have today didn’t even exist 25 years ago. So even as AI replaces workers in some occupations that are manual and repetitive, new job functions will be created.

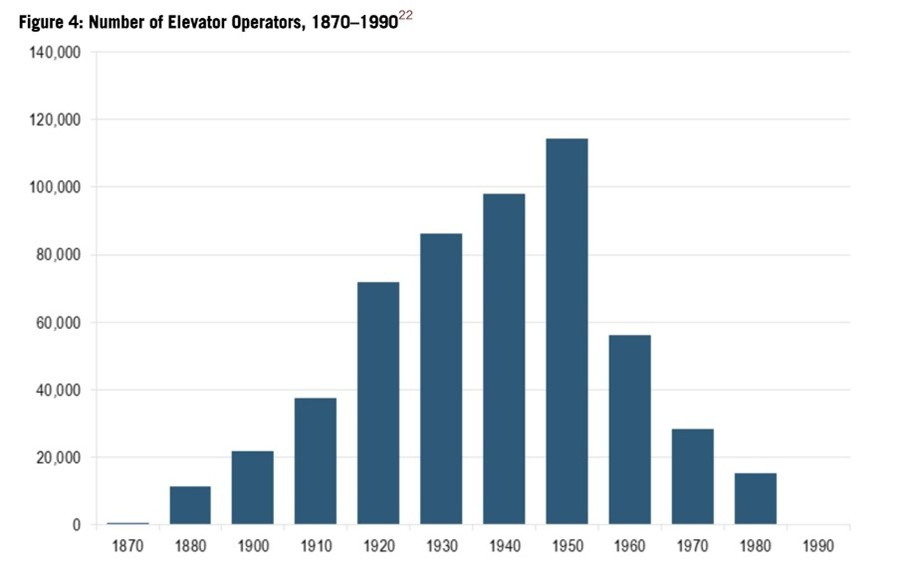

To put this into practice, Dave Kellog makes an excellent analogy to elevator operators, a profession that peaked in the 1950s. Does anybody really miss these jobs?

3. Physical AI is next up for the AI Hype Train

The next wave of AI value won’t live inside SaaS dashboards in web apps. It will extend into robotics, logistics automation, manufacturing, grid intelligence, and industrial inspection. VC investment in robotics soared in 2025 — over $22B deployed, a 69% year-over-year increase — and I’d expect funding to stay strong as companies hit key milestones and investor appetite shows no sign of slowing.

This isn’t just about hardware. World models, led by efforts from Dr. Fei-Fei Li and Yann LeCun, aim to encode the physics and spatial properties of the real world. Many believe this will be foundational to both embodied AI and, eventually, AGI.

A few companies I’m tracking in this space include: Skild AI, Physical Intelligence, RLWRLD and Basetwo.

4. The IPO Window Cracks Open

After a multi-year drought, some of the best-known names in Silicon Valley are gearing up for what could be some of the most anticipated IPOs of all-time. My prediction is at least two names on the list below make their public debut:

Databricks: ~$150B–$220B estimated value @ IPO

OpenAI: ~$830B–$1T+ projected

Anthropic: ~$350B–$500B range

Stripe: ~$180B–$250B

SpaceX: $1T -$1.2 T

None of these are guaranteed — although we know OpenAI and Anthropic have no choice but to tap into public markets soon. Companies with such staggering capital needs can’t stay private forever.

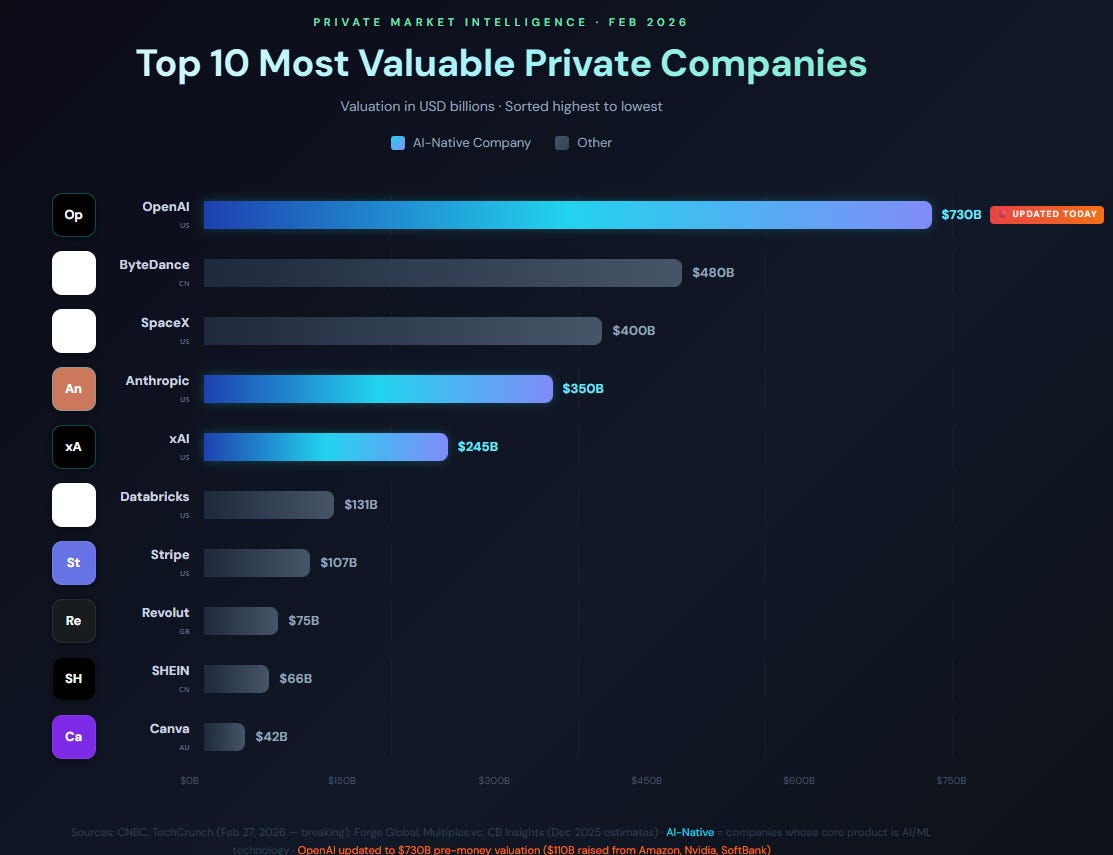

5. AI Bubble Concerns Prove Overblown

Valuations will take their medicine. Capital will get more selective. But real usage and adoption stay firmly intact. This is digestion, not collapse.

For the top AI companies, the fundraising party continues. Looking at the top 10 most valuable private companies, it’s remarkable that 3 of the top 5 are pure-play AI firms. For this elite group of AI companies, I don’t see the music stopping anytime soon.

…however for the other 95% of the market, expect serious cracks appear.

6. Cybersecurity Becomes AI’s Most Defensible Category

In 2026, security will remain one of the most durable and fast-growing categories of IT spend for CIOs in 2026.

AI is both the threat and the solution. It’s expanding the attack surface through model poisoning, prompt injection, and more sophisticated social engineering — but it’s also the primary tool for detecting and responding to those same attacks.

A few categories I’m interested in:

Email + Next-Gen Phishing: LLMs have made spearphishing more scalable and effect than ever. Most legacy tools weren’t built for this new reality.

Security-Focused Frontier Lab: Can a founder build a best-in-class focused entirely on red-teaming models and setting the evidentiary standard the industry needs as LLM built apps become the norm?

Agentic Security: Agents in the Enterprise are getting real credentials and taking real actions. But security is still lacking.

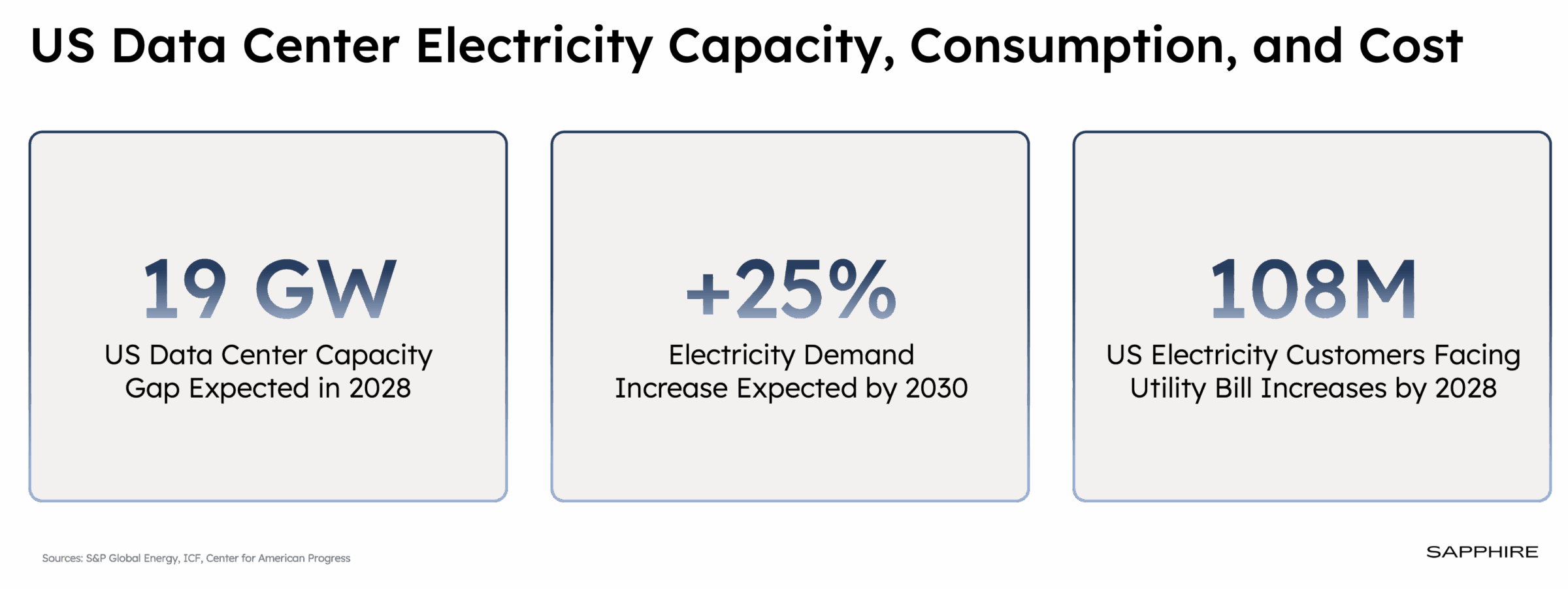

7. Power Becomes the Real Constraint

One of the most underappreciated bottlenecks in the AI buildout isn’t compute — it’s power. Data center energy demand is set to double by 2030, and there’s already an estimated 245 gigawatts of U.S. capacity in development or planning. In 2026, both the physical limits of power delivery and rising political pushback over electricity costs will become major points of contention.

Satya Nadella put it plainly: the biggest issue now isn’t a compute glut — it’s the ability to get builds done fast enough, close enough to power sources. Big tech is already moving aggressively to secure long-term energy, striking deals with decommissioned nuclear plants and entering electricity trading markets.

8. The Application Layer does not become Foundation Model Roadkill quite so easily

Another controversial one! I know it’s trendy to say Clade (which helped me with this) is goint to soon be capable of doing any task and every Cursor-like tool will soon be extinct. But I think AI Apps will prove more resilience than you might think.

Many categories benefit from being *multi-model* and this will force users to continue levreaging multiple providers. Plus, there are many categories where AI startups have built proprietary databases of workflow data from years of execution and are 5x better than the AI labs - Open Evidence (Health), Trullion (Accounting) Harvey (Legal), and Rogo (Finance). So this guy below is flat wrong.

The labs are ambitious and formidable but this is the same as saying Amazon will every online purchase or every search will run through Google.

9. Nvidia Competitors are coming…fast

In 2026, I predict we’ll see many more AI companies manufacturing custom AI chips at scale. We’ve all heard the rumors out of China, where an entire industry has emerged with the sole purpose of displacing the West’s global dominance. New entrants like MetaX and Moore Threads have joined tech giants Huawei, Baidu and Alibaba in the race to produce Nvidia alternatives.

In the US market, mong the first movers will be the large AI labs, for whom purpose-built chips will become increasingly critical part of the stack landscape on which to innovate and compete.

2025 saw VC funding for AI/ML semiconductor companies nearly double, jumping from $4.8B to $8.4B according to PitchBook. Companies to watch in this category include Ricursive Intelligence, Etched, Axelera AI, and MatX.

10. Enterprise AI Budgets Grow — But Consolidate Around Fewer Winners

Companies will increase their AI budgets significantly, but spend those dollars on far fewer vendors.

A TechCrunch survey of 24 enterprise VCs found overwhelming agreement. As Andrew Ferguson of Databricks Ventures put it, enterprises are currently testing multiple tools for single use cases — and in 2026, they’ll cut the experimentation budget and rationalize overlapping tools.

Rob Biederman of Asymmetric Capital was more direct: budgets will increase for a narrow set of AI products with clear results and decline sharply for everything else.

For startups, the implication is clear: if your product isn’t mission-critical by the end of 2026, you’re at risk.

Rapid Fire: A few other predictions I’m making

Here’s my 2026 enterprise AI checklist for separating real adoption from theater:

In 2026, we’ll see the broader shift from seat-based licenses to performance-based economics. AI Agents start getting paid for specific outcomes.

The market finally sours on “Cursor-for-X” copycats, which continue to be undifferentiated solutions in search of a problem (thanks YC!)

Espionage from Chinese’s AI Labs and State-Sponsored enterprises grows 10x, creating a massive industry for Sovereign AI cybersecurity tools

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Investors should do their own due diligence before investing in any securities discussed in this article. This article is based on my opinions and should be considered as such, not a point of fact. Views expressed in posts and other content linked on this website or posted to social media and other platforms are my own and are not the views of NextEra Energy Investments (NEI) or NextEra Energy (NEE: NYSE).

Follow me for more #EnterpriseAdoptionTips

Geopolitics will definitely get more spotlight.

"Espionage from Chinese’s AI Labs and State-Sponsored enterprises grows 10x, creating a massive industry for Sovereign AI cybersecurity tools"