Checking in on First Republic

Analyzing First Republic's troubles and the risk of contagion among US banks

This is my third post on the recent US banking crisis that has already claimed several victims (Silvergate, SVB and Signature Bank) and created shockwaves from Silicon Valley to Wall Street. Check out Part 1 here, and Part II here. Today, we’re going to took at whether First Republic might be the sector’s next victim. If this is your first time receiving this, welcome.

Wild Times for First Republic Bank

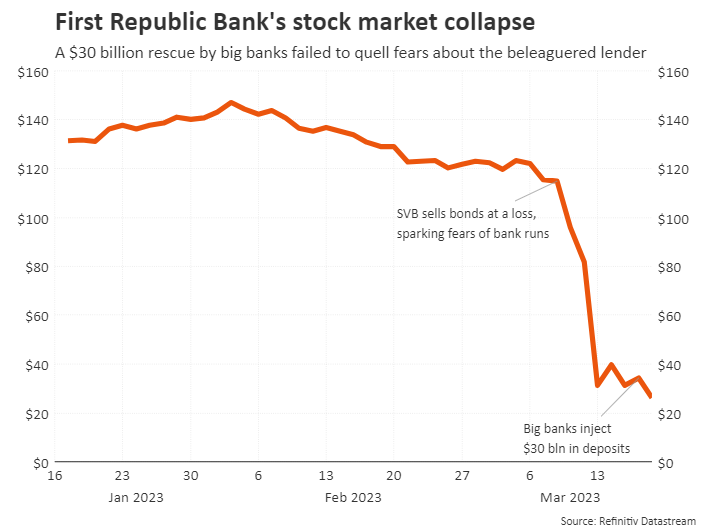

*MONDAY 3/20 UPDATE:* First Republic shares plunged more than 47% on Monday, setting a new record low. JPMorgan is advising the bank on strategic alternatives, including a capital raise or a full sale. The bank has been under immense pressure since the collapse of SVB due to decreasing consumer confidence and its increasingly fragile liquidity position.

First Republic Bank is a well-known private bank that made a name for itself by catering to “low-risk, high-net-worth individuals” (read: millionaires). The bank is also known for its excellent, white glove customer service. Chances are, if you’re a long-time client, First Republic will do almost anything for you.

That’s the good news. The bad news is that, as of writing, the bank’s stock is down over 80% from a month ago, as recent bank collapses have roiled financial markets.

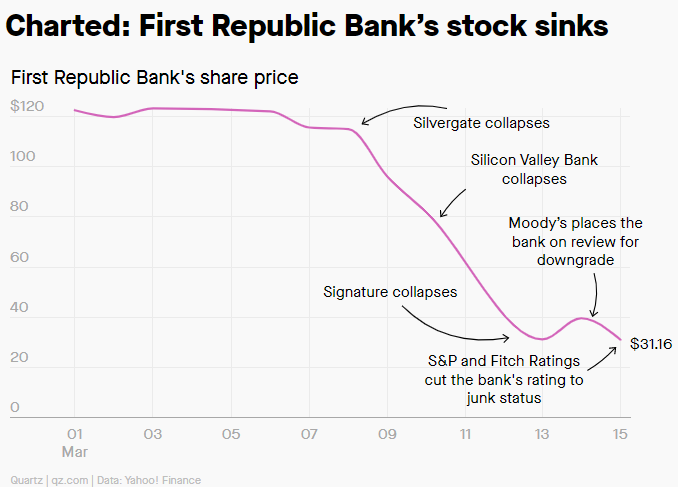

First Republic’s stock just capped off one of the most tumultuous weeks in the company’s 38-year history. The bank saw its stock sink to $19 during trading Monday, rally strongly on Tuesday, only to plunge again over 30% in Thursday pre-market trading. FRB’s stock eventually stabilized Thursday after news broke of a potential rescue from other banks, and shares eventually finished Thursday at $34.27, up nearly 10% for the day. As of Friday end of day, the stock is back down to $23.03.

After SVB and Signature…is FRB next?

When SVB collapsed on March 10, it was the largest U.S. bank failure since 2008 with $209 billion in assets. As fate would have it, First Republic reported roughly $213 billion in assets and $176.4 billion in deposits as of December 31, 2022, making it roughly equivalent to SVB’s pre-crisis size.

The similarities don’t stop there. Investors can’t help but notice parallels between First Republic and the failed Silicon Valley Bank — another regional Bay Area-based lender with a large number of wealthy clients. In particular, while First Republic’s client base is not as concentrated on serving VC firms as SVB, it also has a large number of clients with uninsured deposits. As we’ve learned, when banks have a high percentage of uninsured deposits, the risk of a bank run increases substantially.

Multi-trillion dollar Wall Street banks such as JPMorgan Chase and Bank of America, given their higher share of insured deposits and less risky balance sheets, are unlikely to suffer the same fate as SVB.

But mid-size regional banks simply have less ammunition to weather the storm.

TLDR on First Republic: It’s a privilege to serve you (we hope)

If you’re short on time, here’s a quick rundown of all you need to know about First Republic:

On Wednesday (3/8), SVB announced it had sold bonds at a loss, sparking fears of bank runs. The next day, the four biggest US Banks lost $52 billion in market cap.

On Friday (3/10), Silicon Valley Bank was officially closed by regulators.

On Sunday (3/12), the Fed announced protection for all SVB deposits, both insured and uninsured. The Federal Reserve also said it created a new Bank Term Funding Program aimed at safeguarding institutions affected by SVB’s failure.

Later Sunday, First Republic announced it received additional liquidity from the Federal Reserve Bank and JPMorgan Chase. FRB said the move raises its unused liquidity to $70 billion, before any funding it could get from the new Fed facility.

On Monday (3/13), despite the (seemingly) good news that was announced Sunday regarding its additional reserves, First Republic’s stock dropped 61.8%. This comes after posting declines of 33% over the previous week.

Later on Monday, Moody's placed First Republic and Western Alliance on review for possible downgrade, citing sensitive uninsured deposits, material unrealized losses in its portfolios, and “low level of capitalization” relative to its peers.

On Wednesday (3/15), First Republic’s credit ratings were cut to junk by S&P and Fitch Ratings, amid concern that clients will pull funds from the bank.

On Thursday (3/16), First Republic received a $30 billion pledge from 11 Wall Street Banks. FRB’s stock rallied immediately, closing the day up 10%.

On Friday (3/17), First Republic shares again dropped almost 33%, despite the $30 billion it received the previous day. The bank’s stock was briefly halted during trading Friday, as there were concerns among investors the capital infusion may not be enough to shore up the bank going forward.

Later on Friday, rumors start circulating that FRB plans to raise cash by selling shares privately. Given the current lack of investor confidence, if it does not secure financing over the weekend, there is a chance its shares may free fall on Monday - or worse - fail outright.

Who is FRB and why is it in trouble?

First Republic Bank is a leading private bank and wealth management firm which caters to high-end clients and firms. The company reported more than $212 billion assets at the end of 2022 and generated more than $1.6 billion in net income last year.

However, First Republic has been struggling since the collapse of Silicon Valley Bank last week, as investors have grown increasingly worried about its liquidity. FRB has a high amount of deposits above the FDIC’s $250,000 insurance limit, which makes it “more sensitive to rapid and large withdrawals” (read: bank runs) according to Moody’s.

After the failure of SVB and Signature Bank, the Federal Reserve created a new Bank Term Funding Program that will offer loans for up to a year to banks in return for high quality collateral like Treasurys. In the past week, banks have taken out nearly $165 billion in short-term Federal Reserve loans, taking advantage of two emergency tools to shore up liquidity. But despite the additional capital, investors remain worried.

The Sleeping Giant: Interest Rate Risk

Until recently, the interest rate risk that sleeps quietly on the balance sheets of financial institutions was not something that was widely discussed in venture capital. But more than anything, interest rates are the reason why people are growing increasingly nervous from Silicon Valley to Wall Street.

For a brief period of glorious time, interest rates were effectively zero, so there were not many places to put capital to work. Venture capital firms took advantage of this by raising larger funds, which led to more money being invested into startups, which in turn led to more cash being deposited into banks like First Republic.

Some banks managed this risk well. But others, such as SVB and First Republic, failed to manage this risk appropriately. They invested their excess cash, at low rates, into things like U.S. Treasuries. Once interest rates rose, the value of those bonds declined sharply in value, and banks began to realize they were sitting on large losses.

I’ll have more on interest rate risk in a separate post on this soon.

Moody’s Cuts Rating for First Republic, Puts All Banks on Notice

In a harsh blow to an already-reeling sector, Moody’s cut its outlook on the entire banking system from stable to negative. Yes, that’s right, every US Bank.

We have changed to negative from stable our outlook on the US banking system to reflect the rapid deterioration in the operating environment following deposit runs at SVB, Silvergate Bank, and Signature Bank ~ Moody’s Investors Service

Despite regulators’ efforts to shore up the industry, the rating firm cited interest rate risk as a key factor in its decision. As noted above, an extended period of low rates have created material unrealized losses in securities portfolios across the US banking system. Moody’s expects more banks will come under pressure after SVB’s failure — particularly those with large amounts of uninsured deposits and long-term Treasury bonds that have crumbled in value.

First Republic Bank Cut to “Junk” by S&P and Fitch

On Wednesday March 15, First Republic’s credit rating was cut to junk by S&P Global and Fitch Ratings. Even after US regulators pledged support, the bank was cut to BB+ by S&P and to BB by Fitch, due to concern that clients will pull deposits. This comes after First Republic and other US lenders were already on Moody’s review.

In discussing First Republic, Moody’s called out the bank’s “high reliance on more confidence-sensitive uninsured deposit funding,” high unrealized losses in its bond holdings and a “low level of capitalization” relative to its peers.

Wall Street Banks Pledge $30 Billion of Support

In a sign of confidence in the banking system, a group of financial institutions announced Thursday they had agreed to deposit $30 billion in First Republic.

JPMorgan Chase, Wells Fargo, Bank of America, Wells Fargo, and Citigroup have pledged to contribute $5 billion each, while Morgan Stanley and Goldman Sachs will deposit around $2.5 billion, the banks said in a joint statement. Truist, PNC, U.S. Bancorp, State Street and Bank of NY Mellon will deposit about $1 billion each.

This action by America’s largest banks reflects their confidence in First Republic and in banks of all sizes, and it demonstrates their overall commitment to helping banks serve their customers and communities - Press release issued on behalf of the banks

In a vacuum, this is great news. Regulators say the move by JPMorgan and others demonstrates system’s resilience. But if that’s the case, why has the bank’s stock continued its recent free fall? First Republic’s shares finished Friday down over 32%, showing that investors believe the bank isn’t quite out of the woods yet.

Will there be a similar bank run on First Republic?

From a customer’s point of view, not all deposits are equal. Insured deposits, those which fall under the $250K FDIC limit, are safe. Uninsured deposits, not so much.

The key elements to a classic bank run are: 1) a high proportion of uninsured deposits, and 2) a fundamental loss of confidence in the bank itself, and 3) a crisis which causes customers to panic and make withdrawals simultaneously.

Normally FDIC insurance prevents this from happening. But when banks have a high proportion of uninsured deposits, this changes things considerably. For consumers, it’s every person for themselves. Essentially, whoever tries to take their money out first will be able to get it all out, while the latecomers will lose their money if the bank fails. I covered this phenomenon, known as the Prisoner’s Dilemma, in my last post on SVB.

Effectively, bank runs are self-fulfilling prophecies — as soon as a critical mass of customers believe the bank is likely to fail, they all stampede to pull their money out at once in an attempt to beat the rush. The thinking goes: if you’re not first, you’re last.

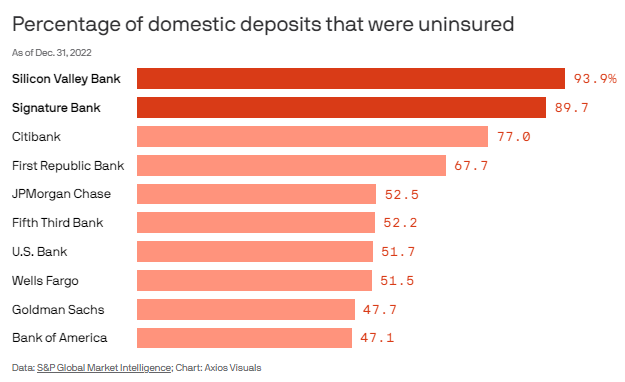

An incredible 94% of SVB’s deposits were not FDIC insured. So it makes sense that it was vulnerable to a bank run. And it may very well become the new textbook example.

So the question becomes: what percentage of First Republic’s deposits are not FDIC insured?

The answer: 68%

At first glance, this number seems like it might be okay. For starters, it’s significantly lower than Silicon Valley Bank and Signature Bank, which both had about 90% of their deposits not covered by FDIC insurance. Making matters worse, SVB and Signature were known for serving two client sectors, venture capital and crypto, that are known for their herd mentality. This greatly compounded the issue.

On the other hand, data from S&P Global shows that, at most banks, about 50% of deposits are FDIC insured. At 68%, First Republic is significantly above that number.

The problem with banks that have largely uninsured deposit bases is that their clients are likely to flee for safer pastures at the first sign of trouble. We saw this happen in last week at SVB, and we very well could be seeing this play out at FRB as we speak.

First Republic Meets the Criteria

As noted above, key elements to a classic bank run, are:

a high proportion of uninsured deposits - Check (not as bad as SVB…but still very much in the danger zone)

a fundamental loss of confidence in the bank itself - Check (have you seen the bank’s stock this week?)

a crisis which causes customers to panic - Check

For those counting at home, we’re officially 3 for 3.

This also helps to better explain why Wall Street Banks came to the rescue with a $30 billion rescue package Thursday - even as the bank repeatedly tried to reassure customers - again, again, and again - that it had more than enough liquidity.

This blog is not financial advice. But if you own any First Republic stock, just remember that shareholders are wiped out completely if the bank fails. Is it really worth the risk?

Anything else we should know?

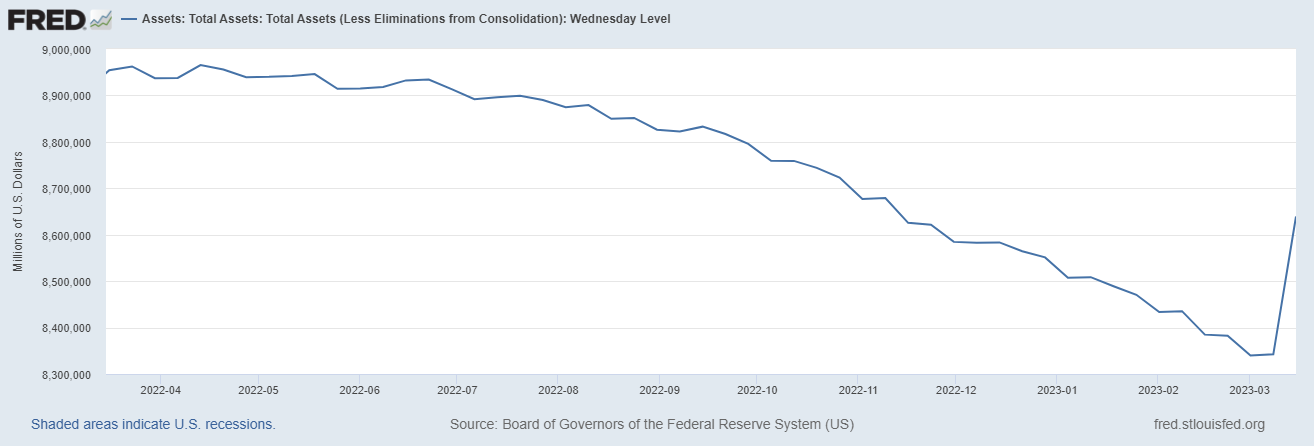

The US Federal Reserve has recently began printing money again. Lots of it.

As you can see in the graph above, the Fed added $300 billion in assets to its portfolio last week. In the last 10 years, the only time Fed has added a larger sum ($0.5 trillion) in a single week was just after we started a global pandemic in March 2020. Yes, we are once again, in unprecedented times.

It’s interesting to note what happened the last time the Fed printed money to this degree. After initially plumetting to less than $5,000 in March 2020, the price of bitcoin multiplied by more than 12x the next year to over $60,000 by March 2021.*

For now, it’s just something to watch. But many are carefully watching to see just how much additional capital the Fed’s new backstop will inject into the system. According to one estimate from JPMorgan analysts, the maximum could rise as high as $2 trillion.

*This is not financial advice. Just an observation!