Fun with VC Data: SaaS Multiples - The Great Valuation Reset

For SaaS startups, yesterday's price is not today's price.

Thanks for tuning into my new blog, Fun with VC Data. Today we’re going to dive into SaaS valuations. Should be fun.

The Great Valuation Reset™

With each passing day that more tech layoffs are announced, and the recession seemingly deepens, a question has constantly popped into my mind:

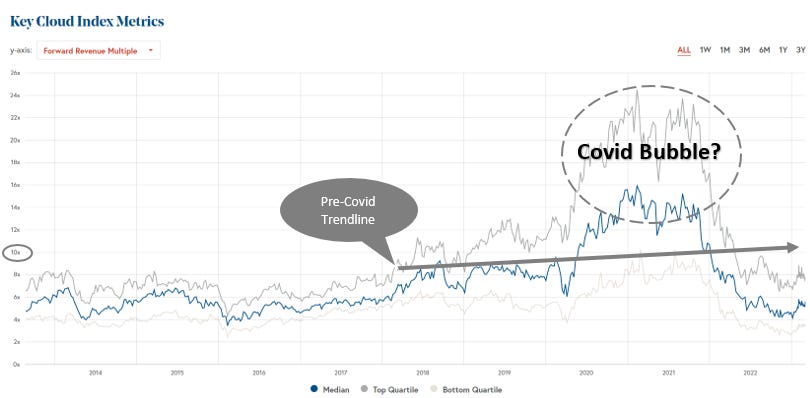

Were the “Covid-era SaaS multiples” just a one-time bubble?

Let’s look at the data.

Based on the historical pre-Covid trendline, we can reach a clear conclusion: Yes, those juicy Covid multiples were likely a one-time thing. You will be missed.

Covid Multiples were Fun

For years, top tier SaaS companies with strong growth received multiples around 10x. Then from 2017-2020, multiples began to perk up. “Hot” startups began to fetch multiples between 15-20x or more. And then in 2021, things got really fun. New data from Pitchbook and IVP reveals that multiples for growth rounds peaked at over 100x (!) ARR during the Covid Bubble.

In 2021, the median late-stage valuation for SaaS deals reviewed by IVP was 114.3x ARR, according to a presentation the firm shared. That multiple expanded more than seven times from the 15.5x ARR fetched by SaaS companies in 2017.

That means ARR multiples for the late-stage SaaS companies rose 700% from 2017 to late 2021. Absolutely insane. Check out the chart below.

In retrospect, 2021 was a crazy time. Competition was fierce. At the time, I remember hearing stories from founders that some Tier 1 VCs - in an attempt to win deals – were offering them term sheets without even first asking to see their financials. That’s like paying all cash for your dream house – sight unseen.

In a frenzied environment where investors were focused on winning deals at all costs – valuation discipline was thrown out the window. And when this happens…well you can probably guess what happens next. Market euphoria ensues, and we see “hot” startups land unprecedented 100x multiples.

Yesterday’s Price is Not Today’s Price

So where do valuations stand today? At every stage, valuation multiples have decreased, making it much harder for companies to raise money.

Why does this matter? Well revenue multiples represent how much VCs and public market investors will value each dollar of revenue. All things equal, a company operating in a sector with higher multiples will find it easier to raise capital.

Moreover, even for startups that have raised recently, multiple compression still poses a big problem as companies look towards their next fundraise, as noted by late-stage investor Meritech Capital in a recent report.

This multiple compression occurring throughout 2022 has had and will continue to have massive ripple effects across the industry. With 70% implied ARR multiple compression, a business must grow its top-line by a multiple of 3.3x to reach the same enterprise value.

The Dangers of Multiple Compression

Whenever a startup receives a rich valuation, you often hear investors justify the mark by saying that a company can simply “grow” into its valuation over time. Sounds good, does the math actually support this?

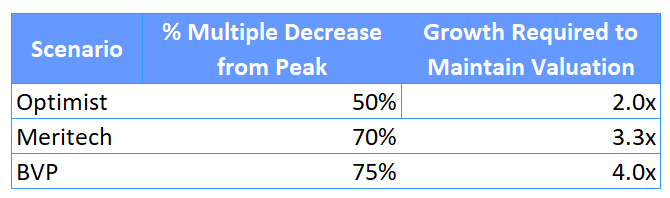

The reality is, for companies that raised at peak of the Covid Bubble, even those with the most runway will have a hard time growing into their valuations. A recent edition of Bessemer’s Parting the Cloud blog summarized things nicely, noting that SaaS multiples were down 75% below previous highs. If each dollar of ARR is worth only a quarter of what it was previously, a startup must grow ARR 4x just to maintain its valuation. Even if you’re an optimist, relatively speaking, and believe multiples are only down 50%, you’d still need to double revenue to reach the same enterprise value.

Closing Thoughts

Despite all the doom and gloom you see on VC Twitter, early-stage venture capital rounds are still getting done today. However, the metrics required to raise capital have greatly increased at all stages (VC Benchmarks coming in a future post!).

Here are a few additional takeaways for founders and investors:

Founder Takeaways

Multiple compression will pose a big problem for companies that raised during the Covid Bubble. Assuming 70% multiple compression, a company must grow 3.3x just to raise a flat round.

To raise capital in today’s environment, you have to be capital efficient.

Expect bridge rounds to become more common, even for startups that have successfully raised capital since 2021.

Investor Takeaways

As recently as 18 months ago, the hottest startups were raising at 50-100x ARR. Those times are gone. 10x ARR is likely to once again the rough standard for SaaS.

For most startups, it will be significantly harder to raise the next round of capital than the last one. VCs should spend more time with their portfolios in 2023, as the average time between rounds has increased significantly.

Beware of the similarities between The Great Valuation Reset™ for SaaS startups and the bubble-like valuations we’re currently seeing for AI startups.

I'm definitely not the target audience for this post! Things went above my head! 😭 But, I eager to put effort to learn and understand.