SVB Bites the Dust

Examining the mess that caused SVB's bank run, who's potentially to blame, and more

Now that we know the Fed has stepped in to save Silicon Valley Bank, I think it’s fair game to look back at how we got here and discuss potential lessons learned.

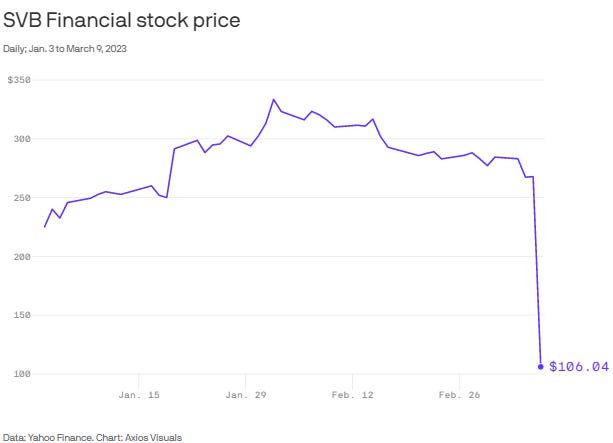

Silicon Valley Bank collapsed Friday, March 10 after a stunning plunge which saw its share price drop 80%, driven by a capital crisis, an all-time PR failure, and an unprecedented bank run that rivals scenes from the Great Depression. In less than 48 hours, it became the second-largest failure of a financial institution in US history.

Gone in 60 Seconds: TLDR on Silicon Valley Bank

Here’s a quick recap of the events that led to SVB’s historic collapse:

In 2021, SVB received a huge influx of deposits which eclipsed the bank’s ability to make new loans. This meant it had lots of excess money lying around. Sounds like a good problem to have right? Well, only if you don’t fumble the bag.

SVB invested all that money, at low rates, into things like U.S. Treasuries and mortgage-backed securities (sounds familiar?)

At the end of February, Moody, SVB’s credit rating agency, informed SVB that it was considering downgrading its credit rating. Knowing that a downgrade would hurt its business, SVB asked Moody’s to postpone the move so it could take action.

On Wednesday, March 8, Silicon Valley Bank announced a $2.25 billion balance sheet bolstering plan, after rising interest rates had caused losses on many of its investments. The plan made sense - it was yielding an average of 1.79% on the securities it sold - but the press release was clunky and poorly worried.

Ironically, despite the moves to clean up its balance sheet, Moody’s ended up downgrading Silicon Valley Bank anyway.

Public investors reacted badly, wiping out more than 80% of SVB's market value.

Its clients, including many venture capital firms, panicked. This led to a bank run of epic proportions. Investors and depositors reportedly initiated withdrawals of $42 billion (!) in deposits from SVB on March 9, 2023. Not great.

Once the bank’s capital-raising attemps failed, SVB started actively seeking a buyer. But there were no takers on such short notice.

By Friday morning, Silicon Valley Bank was officially closed by regulators, which are now in charge of the bank’s deposits. Insert: FDIC.

On Sunday March 12, the Fed announced protection for all SVB deposits, both insured and uninsured.

What Caused this Mess?

For those interested, here’s a deep dive on what happened at Silicon Valley Bank:

***Spoiler alert: everyone did not stay calm***

Who is SVB?

Silicon Valley Bank (SVB) was for a long-time the leading bank for startups, venture capital firms, as well as other businesses. Founded in 1983, the Santa Clara-based bank was also a pioneer of venture debt, a type of loan specifically designed for startups. Venture debt is a crucial lifeline for many VC-backed startups as they are not eligible for traditional bank loans due to their financial profile (i.e., they are not profitable). Effectively, Silicon Valley Bank provides lots of services to startups that other banks won’t touch. This made it extremely popular.

Part of SVB’s problem is they have a major branding issue in the media. Let’s just call it what it is. There may not be a less socially acceptable company to “bail out” than one called Silicon Valley Bank (even if a Fed guarantee ≠ bail out). There are lots of people that feel SVB "is getting what it deserves" here. I am not one of them.

Exhibit A:

This crisis has revealed that a large portion of Americans: 1) don’t understand how crucial SVB was to modern innovation, and 2) believe that SVB was the bank of rich venture capitalists and Big Tech companies. Like many things in 2023, SVB has become just as much of a political issue as anything else. But remember, if startups can’t make payroll, lots of regular working people won’t get paid. VCs will be fine.

SVB by the Numbers

With more than $209 billion in assets as of December 31, 2022, SVB’s collapse is the second-largest bank failure in history, trailing only that of Washington Mutual and the largest since the 2008 financial crisis.

SVB was the 16th-largest bank in the US at the time of its failure.

Nearly half of US VC-backed technology and life science company have a banking relationship with Silicon Valley Bank.

From 2019 to late 2022, SVB’s total deposits grew more than 3x. This compares with industry deposit growth of “only” 37% over the period.

Current List of Companies with Silicon Valley Bank, $SIVB, Deposits:

The Kobeissi Letter@KobeissiLetterCurrent List of Companies With Silicon Valley Bank, $SIVB, Deposits: 1. Circle: $3.3 billion 2. Roku: $487 million 3. BlockFi: $227 million 4. Roblox: $150 million 5. Ginkgo Bio: $74 million 6. iRhythm: $55 million 7. Rocket Lab: $38 million 8. Sangamo Therapeutics: $34 million… https://t.co/KD0O5FCq3y5:23 PM · Mar 11, 20234.68K Reposts · 14.7K Likes

The Kobeissi Letter@KobeissiLetterCurrent List of Companies With Silicon Valley Bank, $SIVB, Deposits: 1. Circle: $3.3 billion 2. Roku: $487 million 3. BlockFi: $227 million 4. Roblox: $150 million 5. Ginkgo Bio: $74 million 6. iRhythm: $55 million 7. Rocket Lab: $38 million 8. Sangamo Therapeutics: $34 million… https://t.co/KD0O5FCq3y5:23 PM · Mar 11, 20234.68K Reposts · 14.7K Likes

Prisoner’s Dilemma that Drove SVB’s Bank Run

Earlier in this post, I outlined the steps that triggered the collapse at Silicon Valley Bank. After a period of low interest rates, the Fed raised rates in an effort to curb inflation. A large portion of SVB’s investment portfolio was suddenly underwater, just as VC funding for the startup clients that SVB serves started to dry up.

With SVB facing mounting pressure to shore up its balance sheet, or risk getting downgraded by Moody’s, the bank announced plans to raise capital, sending its public stock into freefall. Once news of a “bank run” reached Twitter, investors advised their portfolio companies to pull funds, and the entire system collapsed overnight.

In many ways, the SVB situation resembles a classic Prisoner’s Dilemma.

Examining the Prisoner’s Dilemma

The Prisoner's Dilemma is a thought experiment from the 1950s where two suspects are asked to betray one another in exchange for lesser sentences. However, if both refuse to cooperate, each would be better off.

Similarly, if all SVB customers had remained calm and kept their funds in place, the bank likely would’ve been fine. But for most stakeholders, there was little zero downside to pulling at least some of your funds from SVB, and huge potential upside. Clients could secure funds that would otherwise be frozen (a risk given payroll and other near-term obligations) or lost forever.

The unfortunate consequence of SVB’s collapse is that most startups will now be much worse off from a banking perspective, as there will be greater risks (and costs) throughout the financial system.

Who’s Fault is This?

In situations like this, people always are quick to place blame. In this case, however, SVB’s collapse cannot be traced down to a single guilty party. As I outlined above, it was a series of decisions that ultimately led to SVB’s demise.

BUT JUST FOR FUN. Here are some of the parties getting most of the blame for SVB’s collapse…

SVB Management Team

While the Fed announced that SVB’s depositors will be fully protected, SVB executives should’ve never put their customers in this position.

In fact, SVB’s management team failed its clients and investors in two key ways:

Mistake #1: Risk Management and Lack of Diversification

Most of the blame falls on SVB itself. The management team failed to manage interest rate risk entirely and clearly did not pay attention to their LCA or FRC classes at Harvard Business School. My old professors are likely writing new cases as we speak.

Silicon Valley Bank violated one of the elementary rules of finance: Always diversify. ~James Surowiecki, Fast Company

Mistake #2:

BadAbsolutely Horrible Corporate Communication

Even despite its regrettable error in risk management, SVB had enough liquidity to cover a normal rate of withdrawals. However, when it announced its plan last week to bolster its balance sheet via press release, it had a few notable omissions.

As Lulu Meservey (Activision CCO) notes, SVB failed to actually explain why they were raising capital. Even worse, it failed to control the narrative and reassure its customers that it still had a strong balance sheet. When Silvergate collapsed, it triggered worries that SVB might also be in trouble. This caused its clients, including many venture capital firms, to start panicking, which leads me to my next point.

Venture Capitalists

Greg Becker, SVB’s CEO former CEO, hoped the trust and brand equity SVB had built over the years with VCs would protect it from last week’s events. He was wrong.

To be fair, he wasn’t completely wrong. Many VCs wanted to help SVB.

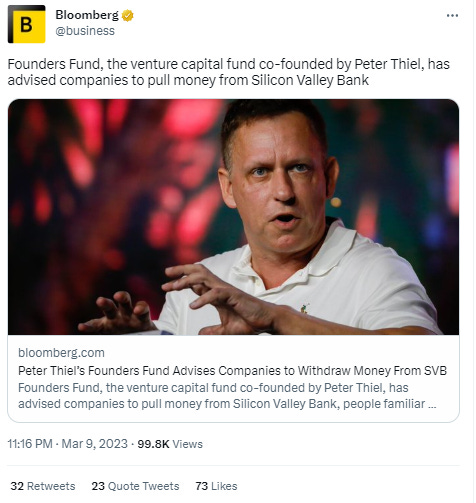

But the startup world holds certain VC and Tech influencers in extremely high regard (see: Musk, Elon), and more importantly, tracks their every move with extreme intensity. And it only takes one. So when Peter Thiel’s Founder Fund advised its companies to pull money from SVB, a lot of founders and other VCs followed suit.

The Founder’s Fund news created a firestorm. Because most of SVB’s customers belong to a very small community that’s always on social media, it was hard to miss.

And this was just the tip of the iceberg. Some VCs chose to fan the flames by *TWEETING IN ALL CAPS* causing further panic and more withdrawals (iykyk).

So, despite Becker’s warnings to “stay calm”, given the Prisoner’s Dilemma at play, many had no choice but to quickly withdraw money. It simply wasn’t worth the risk.

It certainly makes you wonder, without Twitter and social media, would this bank run have even happened?

The US Government

Some blame the Fed for raising interest raises excessively in an attempt to combat inflation. SVB invested heavily in US government bonds as its deposits swelled, so when the Fed later raised rates, the value of its bonds dropped significantly.

Personally, I think this is a lazy take (perhaps SVB shouldn’t have gone without an official chief risk offer for 8 months?). But it still makes for a great meme.

What Happens Next?

The next few weeks and months may be difficult. Silicon Valley Bank and Signature Bank have been shut down, which means layoffs are coming. Many organizations will be restructured in the coming months, and the ripple effect will impact many organizations across tech and finance. Already, Y-Combinator announced that they are cutting nearly 20% of staff and scaling back late-stage deals.

Potential Silicon Valley Bank Alternatives

Disclaimer: Please do your own research. This is not financial advice and I do not personally use hold investment interests in any of these startups. And remember: diversification is key.

Large Banks (safer yes, but are slow and often low-tech. also…keep in mind, the minimums can be quite high): JP Morgan Chase, Wells Fargo, BofA, etc.

Regional Banks (proceed with caution): First Republic Bank (closest comp to SVB, but comes with risk), PacWest,

Signature Bank(welp)VC-Backed Startups: Brex, Novo, Grasshopper, Mercury* (I’m a little suspicious by the sponsored ads right after a catastrophe - but many startups do use them)

Venture Debt (stick with the biggest players): Hercules Capital, WTI, Runway, etc.

Reminder: Check on your Founder Friends

Remember, running a startup is very hard, and recently founders just can’t catch a break. So do yourself a favor and go check on your startup friends. This has been a nightmare week, and they’ll likely appreciate it more than you can imagine.