The AI Bottleneck Isn't Chips. It's Watts.

Why the next era of AI will be defined by power, not silicon

Scaling the Enterprise · Part II of a Series on AI’s Cost-Accounting Era

Key Findings

Anthropic and OpenAI together are valued at roughly 2x the combined market cap of the 10 largest US investor-owned utilities. The market is pricing intelligence as the scarce resource. But is it?

The US has not executed a coordinated, national-scale grid buildout in roughly 50 years. We’re now asking that same grid to absorb the largest industrial load growth in a generation.

JP Morgan estimates $1 trillion of US grid investment is needed over the next decade. But the constraint isn’t dollars — it’s time. The average new transmission line takes 10+ years to build.

Chip efficiency has been the bottleneck on AI economics for the last three years. My POV is that grid capacity will be the bottleneck for the next 10.

Data-center electricity demand is skyrocketing, with AI the biggest driver. Access to firm power will be the biggest competitive advantage in the AI race.

The AI Bottleneck isn’t Chips. It’s Watts

2026 saw OpenAI announce a $122 billion fundraise at an $852 billion valuation. Anthropic followed with a $65 billion raise at a $965 billion valuation. Between the two, they’re now worth roughly twice the combined market cap of the ten largest US investor-owned utilities.

The companies selling intelligence are valued at a multiple of the companies selling the electricity required to produce that intelligence. The market believes the battle for AI supremacy is a contest between Nvidia, Anthropic, and other technology giants. But the AI race is quietly becoming a race for electricity, not chips.

Last week I wrote about how CEOs are pushing back on AI spend and why the application layer is heading into a cost-accounting era.

That post focused on the demand side:

Because right now, enterprises are doing some deep soul searching to determine whether token consumption actually translates to business outcomes.

Today’s post focuses on the supply side: AI cost conversations in board rooms are quickly becoming energy conversations. And right now — the math ain’t mathing.

My hypothesis is simple: chip efficiency and compute has been the bottleneck for the last three years. Grid capacity will be the bottleneck for the next ten.

I: US Power Grid: The Largest Machine on Earth

Universally available, reliable, and affordable electricity is taken for granted.

But delivering power to 350 million people in the United States is no easy feat. The American power grid is the largest machine on Earth — roughly 7 million miles of transmission and distribution lines, 240,000 miles of high-voltage backbone, and more than 180 million power poles. Concerningly, in the early 2010s we added 1,700 miles of new high-voltage transmission per year. Today, we’re adding 350. So what gives?

A grid that nobody fully owns

Quick: who runs the American power grid?

Trick question. Nobody does.

There is no National Grid Authority.

The US power grid has evolved from Thomas Edison’s localized 1882 Pearl Street Station into a massive, interconnected network. Today, it functions as one of the world's most complex engineering feats, a massive, complex industry that works in harmony to deliver power to consumers.

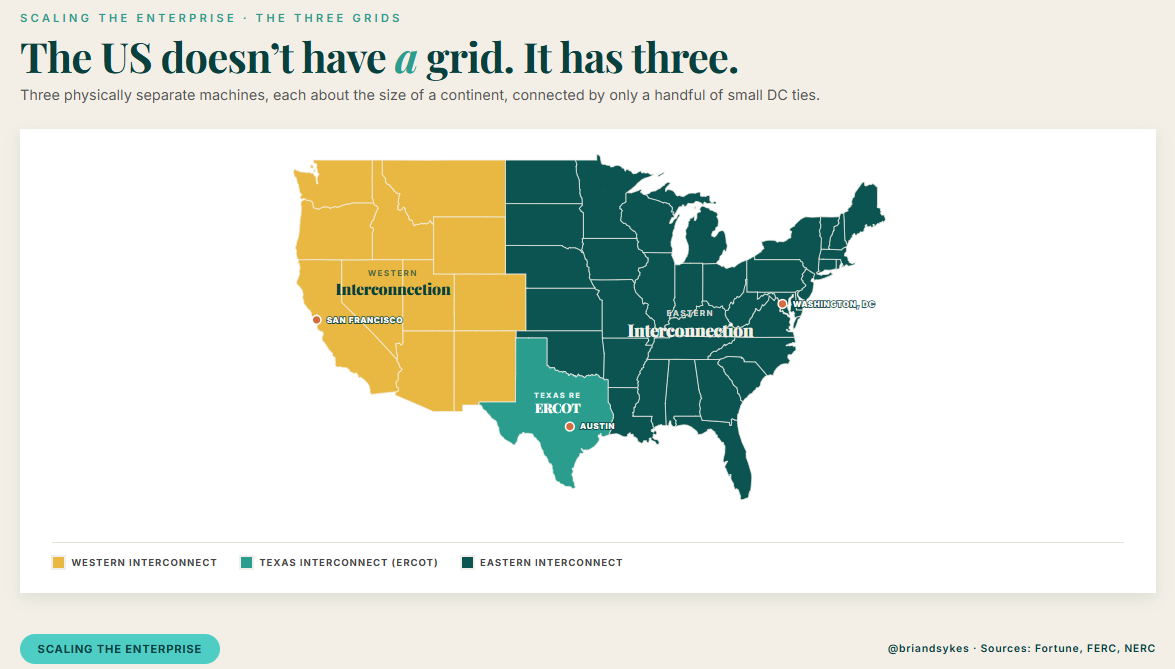

The United States doesn’t have a grid. It has three.

That’s right, the Eastern Interconnection, the Western Interconnection, and ERCOT, which covers most of Texas, are physically separate machines. Each of them is about the size of a continent, connected by only a handful of small DC ties. When a 2021 storm took down Texas, ERCOT could pull only ~6% of its peak demand from its neighbors. The result was the largest deliberate electricity shutoff in US history.

Inside the three grids, things get more fragmented. Seven regional operators — PJM, MISO, ERCOT, CAISO, NYISO, SPP, ISO-NE — coordinate roughly two-thirds of the country. The rest is run by individual utilities making their own decisions about generation, transmission, and who gets connected when. Large parts of the Southeast, Northwest, and Southwest have no formal wholesale power market at all.

Layer on roughly 3,000 utilities, 50 state public utility commissions, and one federal regulator (FERC) with limited authority over retail markets, and what you have is less a system than a federation of systems that mostly agree to keep the lights on.

It works, most of the time, because everyone behaves. But here’s the issue: the grid was not designed for anyone to add 50+ gigawatts of new industrial load in five years.

A grid older than most of the people running it

Most of the high-voltage backbone you see on a map today was built between 1950 and 1975. That backbone has been carrying power for fifty to seventy years. The average large power transformer in the US is roughly forty years old. Many of the substations being asked to serve modern hyperscalers predate the personal computer.

This is not a knock on the equipment — utility-grade hardware is built to last, and most of it does. But “keeping the lights on” and “expanding production” are two very different stories. And we need to significantly ramp capacity. So how do we do it?

The mechanisms for actually upgrading the system are slow. Permitting new transmission lines can take over a decade. Connecting new generation to the grid currently averages five-plus years and growing. There is no national grid authority that can compress the timeline; every project negotiates separately with state regulators, local landowners, and the utility on the other end of the line.

This is the part that people in the AI world tend to underestimate. You can spin up a Kubernetes cluster in an afternoon. You cannot spin up a 765-kV transmission line.

A grid getting greener and dirtier at the same time

The most interesting thing about the US energy mix right now is that it is moving in two directions at once.

In March 2026, renewables generated more US electricity than natural gas for the first time. Combined with nuclear, clean sources supplied more than half of all US power. Solar, wind, and batteries are projected to account for 93% of new capacity added to the grid this year, per EIA. The transition is real and accelerating.

At the same time, AI demand is keeping coal alive. Nine coal plants scheduled to retire last year had their operating lives extended, five of them under emergency orders from the Department of Energy. The White House has made its opinion on coal clear. Total coal capacity retired in 2025 was the lowest in fifteen years.

So how can both things be true? It’s because new megawatts are mostly green, but old megawatts are running longer than anyone planned. The grid we have today is more renewable, more fossil, and older — all at once.

This is the system we are now asking to underwrite the next decade of AI demand growth. Reinforcements are needed. Quickly.

II: The Challenge Ahead

To meet surging electricity demand, significant grid infrastructure will need to be built and upgraded over the next decade.

Trillions of dollars are expected to flow into AI infrastructure over the next few years. JPMorgan estimates $1 trillion of US grid investment alone is needed over the next decade — $5.8 trillion globally. Those are big numbers. But the real question is, how long will it take to get that capital deployed?

The average new transmission line in the United States takes more than ten years to permit and build. Per recent New York Times analysis of FERC data, the interconnection queue currently holds more than 2,600 gigawatts of generation and storage waiting to connect — roughly twice the size of the entire installed US generation fleet. Average wait time in the queue has grown from less than two years a decade ago to more than five years today.

Meanwhile, the AI buildout is being announced on a different timeline. Every frontier model and AI chip release feels like a sprint. Announcements for new data center projects happen almost as frequently - with projects getting increasingly massive in scale. Project Stargate alone targets nine-plus gigawatts across seven US sites.

AI Data Centers Pushing the Grid to the Limit

The scale of AI data centers and their commensurate power needs are growing exponentially. To make the point more clear: a single gigawatt-scale campus needs more new firm power than most US states have added in the LAST DECADE.

A 1 GW AI data center consumes the equivalent power of roughly one million US households and requires $10B+ in upfront investment.

To meet growing AI demand, the semiconductor industry is constantly churning out increasingly powerful chips, which in turn requires a new generation of power-hungry data centers that are set to overwhelm our aging grid infrastructure. There’s a real risk that we run out of power before we can actually serve all of this demand.

The reason is simple: these AI data centers are using more power than ever.

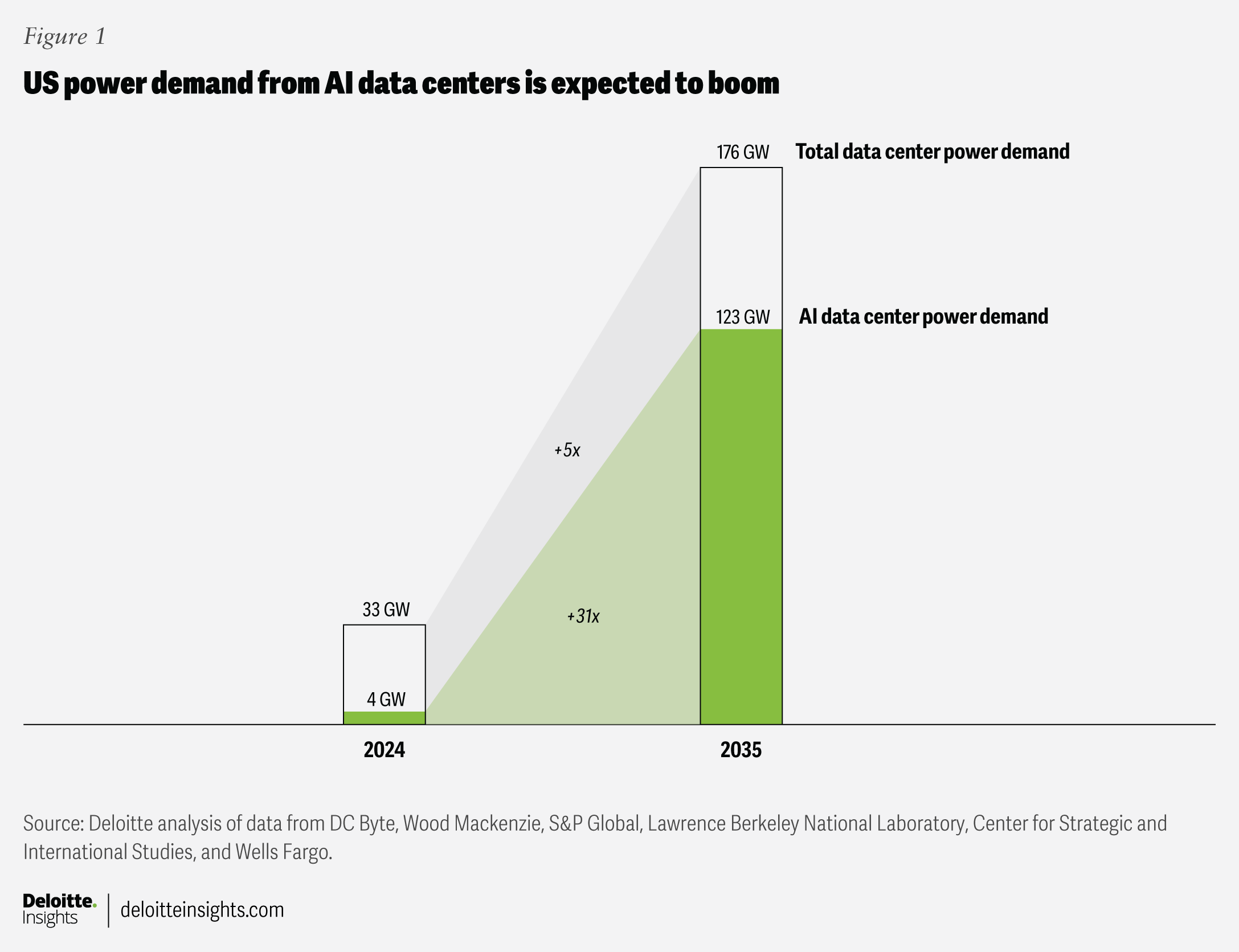

By 2035, Deloitte estimates that power demand from AI data centers in the United States could grow more than 30x, reaching 123 gigawatts, up from 4 gigawatts in 2024.

The real constraint on AI is no longer talent or chips. It's power. The best models in the world are worth nothing if you can't plug them in.

III: While Everyone Fights Over Tokens, the Smart Money Is Buying Watts

There are two AI races happening right now. Only one of them is making headlines.

The Race for Compute

This is the visible race that everyone loves to cover: GPU allocation, model benchmarks, frontier capability, who gets API capacity first. It plays out in quarterly product launches and investor decks. It is loud, fast, and largely commoditized — every player is fighting over the same scarce inputs and the same downstream customers, and the gap between first and tenth place narrows every quarter.

The Race for Electrons

The silent race is the one a handful of players figured out 18-24 months ago. They stopped buying inference and started buying electrons.

The largest AI buyers are treating electricity like a top strategic priority. They are getting more sophisticated with offtake agreements, M&A, land purchases, and in some cases even choosing to vertically integrate with power producers outright. Effectively what they are doing is converting a variable cost — electricity at whatever the spot market clears — into a fixed cost at known prices.

A new model is emerging: data centers supplying or acquiring their own power. Tech companies are increasingly building or contracting for dedicated energy resources to secure faster access to electricity and reduce pressure on the grid.

The Smart Move: “Bring Your Own Power”

In a stable demand environment, this wouldn’t matter. In a power market where power costs are spiking faster than anyone expected, this has the chance to become the single most important strategic move in the industry.

Four things follow from securing your own power:

You control your own destiny. A company that has signed long-term PPAs for its compute is no longer a passenger on someone else’s grid. It does not need to stress about waiting in line for interconnection. It can focus on its business.

You control your own margins. Power is the single largest variable cost in AI inference. Locking it in is the equivalent of what airlines did with jet fuel hedges or what Amazon did with logistics: take the input most exposed to inflation, fix the price for a decade, and let everyone else pay spot.

You secure long-term capacity. This is the one nobody talks about. New gigawatt-scale generation projects take five to ten years to bring online. The capacity for 2030 is being contracted as we speak.

You move before the window closes. Every quarter that passes, the menu of available generation shrinks and the prices climb on what remains. With each passing day, counterparties also get much pickier about who they’ll sign with.

Now look at the AI application layer companies. They are buying inference capacity from hyperscalers at market-rate. They have little leverage. Their cost of goods sold is fully exposed to whatever the underlying power market does over the next decade.

No app layer AI company breaks out electricity costs as a line item. But if they did, it would tell an interesting story about who truly has a competitive advantage, and who has a serious margin problem.

In my view, the AI companies that survive the cost-accounting era will be the ones that understand that firm-power can be a strong moat.

IV: A Wake-Up Call

For nearly two decades, US electricity consumption was flat. That era is over. U.S. electricity demand is experiencing its first sustained, nationwide surge in years.

How the AI Race Might Bring Necessary Changes

The AI buildout may end up being the catalyst that finally funds the grid investment America has been deferring for fifty years. The time to act is now. The New York Times recently framed data centers as “a wake-up call” for a system that is “too old” with electricity supply that is “too small.”

That’s not a crazy take. It’s also exactly why the firm-power moat matters — the companies that locked in capacity before the wake-up call are the ones who benefit most from it. The reckoning is what makes their position valuable.

There are significant risks of not acting now.

Power emergencies are now routine; the federal government declared one during a recent heatwave. Supply chain bottlenecks, permitting delays, rising costs, cybsecurity threats and hardware shortages are among other risks to weigh.

Final Thoughts

The AI industry has spent three years optimizing for chip efficiency, model architecture, and inference cost per token. Those optimizations have produced a 90%+ decline in the price of intelligence and an even larger increase in its consumption.

The next 3-5 years will be different. The bottleneck is moving from silicon to substations, from inference to interconnection, from what Nvidia ships to what local utilities can actually deliver. The companies that recognized this early and locked in capacity before the wake-up call are the ones who will benefit most.

Scaling the Enterprise · A Series on AI’s Cost-Accounting era

Next week (Part III): The cost of renting intelligence: How enterprises can use open-source to build custom intelligence instead of relying on frontier models.

Coming soon (Part IV): If power is the bottleneck, where does the venture capital go? Mapping the investable themes at AI × Energy.

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Views expressed are my own and should be considered as such, and are not the views of NextEra Energy Investments (NEI) or NextEra Energy (NYSE: NEE)

Thank you for the article!

There is nothing that compares to looking at a load/demand curve over the last decade in Northern Virginia. It looks like a hockey stick.

Now, I do think that despite moving away from conventional power generators to something like micronuclear reactors or other forms distributed generation will necessarily make power flow models more complex. And not just complex in the number of interconnected components, but also in their nature. A mix of typical rotating machines and inverter based resources is already introducing weird dynamics in the grid that have been previously unseen, and those could cause catastrophic failures if not noticed on time (and they almost never are).

We truly live in a very interesting age for the power systems and power grids across the globe. The US grid proves to be yet again one big unprecedented case study.

This is great.

I do think we will have alternatives to transmission lines within the next 5-10 years. Think nano-electric fluids that decouple power and energy and allow for transport in conventional ways.