The Market Map: Owning Your Intelligence

Mapping the ecosystem enabling enterprises to build and own AI

Scaling the Enterprise · Owning Your Intelligence, Part III, Vol. 3

Most enterprises have never heard of Mercor, Applied Compute, or Fleet. But when Cursor spent 85% of its training compute on post-training and RL rather than pretraining, it showed the importance of this layer for modern AI teams. The good news is that you don’t need to be a $60B coding startup to access RL Gyms. In fact, there’s now a thriving ecosystem of companies that enterprises can readily use.

This is Part III of the Owning Your Intelligence series. Part I made the case: the era of renting intelligence from frontier APIs is ending, and the enterprises that own their own models will compound faster than those that don’t. Part II showed how to do it — the post-training playbook, the role of RL, and the domain model builders who’ve already run this experiment and won. Part III maps the companies you need to know. It introduces six key categories spanning AI infrastructure, training specialists, and bespoke AI training data providers that make intelligence ownership possible.

The market behind the map

A few statistics worth knowing before diving in:

AI training data is a $3.4 billion global market in 2025, projected to more than double to $8.3 billion by 2030 — a category that barely existed a few years ago.

Reinforcement learning infrastructure sits at $12–15 billion today and is expanding at 28–35% annually. The RLHF platform segment specifically — the pipelines that turn human feedback into reward signals — is projected to grow from $2.8 billion to $18.6 billion by 2034.

Enterprise post-training adoption has crossed a meaningful threshold: 67% of Fortune 500 companies have already completed or initiated at least one domain-specific fine-tuning project. The question is no longer whether enterprises will post-train their own models. It’s who in this ecosystem they’ll use to do it.

For a recap of the benefits of owning your intelligence, check out Part 1 of my series below:

The End of Renting Intelligence

We are entering an era of token scarcity and rapidly shrinking gains from each new frontier model release. Why leading companies can no longer afford to rent frontier intelligence

Owning Your Intelligence Market Map

Owning intelligence isn’t a weekend do-it-yourself project. It requires serious tools and infrastructure. That’s why a fast-growing ecosystem of startups provides the infrastructure, training environments, real-time knowledge systems, and foundation models that let enterprises post-train and deploy custom AI without building a frontier research lab.

Introducing: The Market Map

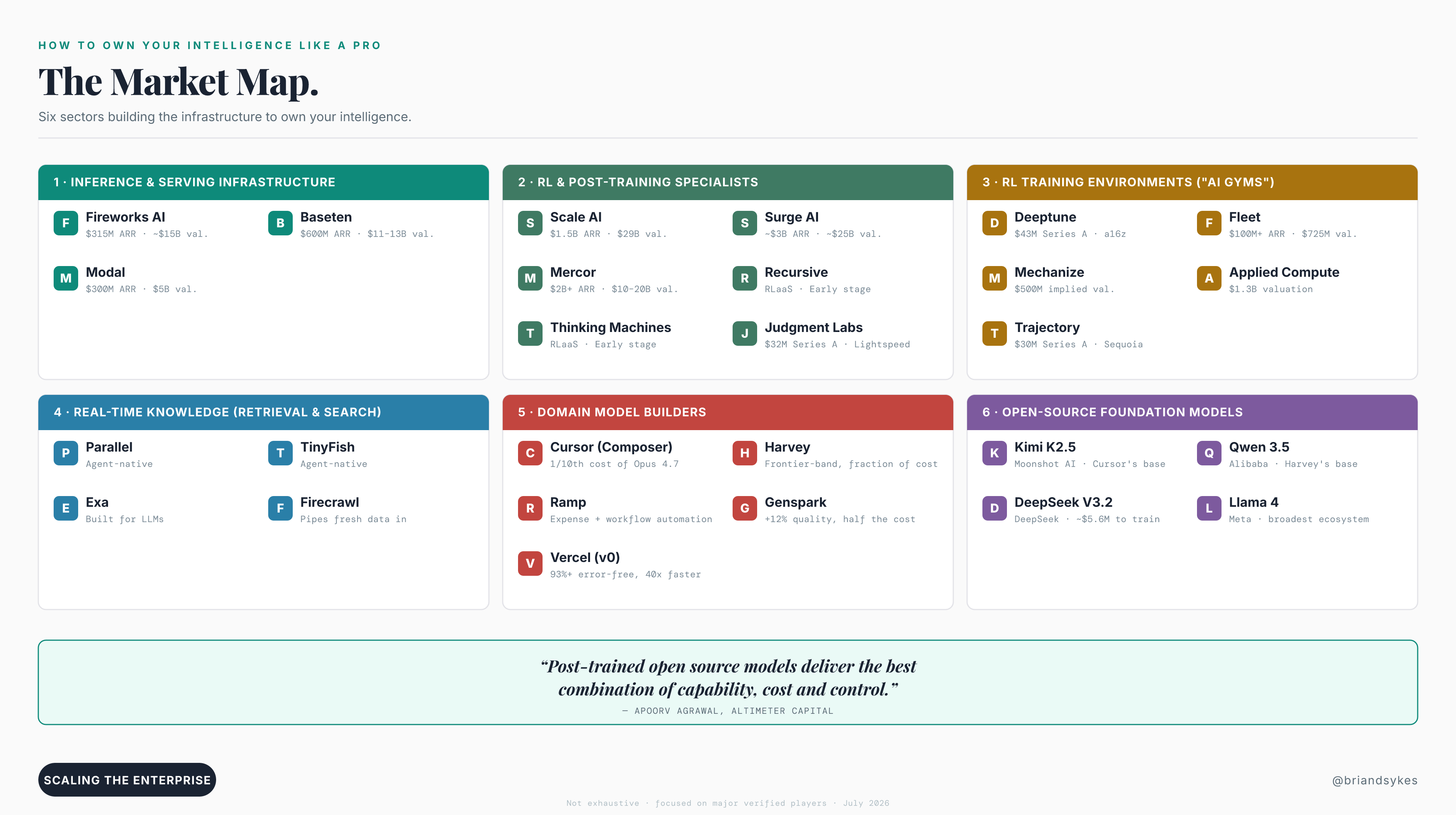

Breaking Down the Map: Six Key Categories

Menlo Ventures recently catalogued the AI training data and RL environments market: more than 50 companies generating roughly $8.5 billion in combined annual revenue. More than 75% of that revenue flows to just four players — Scale AI, Surge AI, Mercor, and Handshake — but the remaining $2+ billion is spread across dozens of specialized infrastructure companies building what the next decade of AI will actually run on. While the overall landscape is too large to capture perfectly, the six categories below encompass most of the major players.

1. Inference & Serving Infrastructure

The layer that runs deployed custom models at scale.

Fireworks AI — The infrastructure story of the year: $315M in annualized revenue as of February 2026, up 416% year-over-year. Reportedly in talks to raise at a $15B valuation, a 3.75x jump from its $4B Series C just seven months earlier. The company offers training and inference under one roof. CEO Lin Qiao’s thesis: “Not just consume intelligence. Own it.”

Baseten — Infrastructure hardening into a category. $300M Series E at a $5B valuation in January 2026; Q1 2026 revenue tripled in a single quarter to roughly $600M ARR. That round closed in June 2026 as a $1.5B Series F led by Altimeter Capital, Conviction, and Spark Capital, priced across two tranches at $11B and $13B. This tripled Baseten’s valuation in less than five months.

Altimeter’s Apoorv Agrawal, who led the investment, frames the thesis around inference demand: “Post-trained open source models deliver the best combination of capability, cost and control.” Built for high-throughput production serving, especially agentic workloads at scale.

Modal — $300M raised at a $5B valuation, with $300M in ARR. Developer-first and maximally flexible — the choice for engineering teams that want control over how their models run in production without trading that control for a managed service.

2. RL & Post-Training Specialists

The teams that run the training process.

Scale AI — The dominant platform for AI training data and RLHF pipelines: the layer that turns raw human feedback into the reward signal post-training runs on. $1.5B in annualized revenue at a $29B valuation as of 2026. Most frontier labs and a growing number of enterprise post-trainers run on Scale’s data infrastructure.

Surge AI — One of the largest human-in-the-loop training data providers, running contractors and annotators at the scale frontier labs need to run RLHF. ~$3B in annualized revenue at a ~$25B valuation as of mid-2026 — making it one of the fastest-scaling companies in the AI training stack.

Mercor — AI-native talent marketplace that matches and manages the human contractors who run reinforcement learning pipelines. $2B+ in annualized revenue, with the company in talks to raise at a $10–20B valuation. From $1M to $1B ARR in roughly 20 months — one of the fastest revenue ramps in the category.

Recursive and Thinking Machines — Building RLaaS (Reinforcement Learning as a Service) platforms, the abstraction layer that lets enterprise teams run post-training workflows without standing up their own RL infrastructure. Both early-stage but backed by investors who treat RLaaS as a distinct infrastructure category rather than a feature of the inference stack.

Judgment Labs — Agent evaluation and observability infrastructure for post-trained models: the tooling that lets a team build the kind of private eval rubric this piece argues every enterprise needs before it can trust a custom model in production. Raised a $32M Series A led by Lightspeed in May 2026.

3. RL Training Environments (”AI Gyms”)

Platforms that give agents a safe place to learn before production.

Deeptune — Builds high-fidelity simulation environments where AI agents practice complex digital workflows before touching production — a flight simulator for enterprise AI. Closed a $43M Series A led by Andreessen Horowitz in January 2026.

Fleet — Builds RL environments for messy enterprise workflows specifically: legacy systems, inconsistent data, and the edge cases that synthetic training environments tend to miss. Now at $100M+ ARR with a $725M implied valuation — the fastest-growing pure-play AI gym.

Mechanize — Builds reinforcement learning environments designed to automate complex knowledge work at scale, training agents on the kinds of tasks that have historically required human judgment.

Applied Compute — Embeds RL engineers directly with enterprise customers, turning product usage data and eval traces into continuously improving models. Decentralizes intelligence by training smaller, highly customized, cost-effective models on a company’s own data. $1.3B valuation.

Trajectory — Rumored to be raising a $30M Series A led by Sequoia to build a continual learning platform. Similar to Applied Compute, company’s central thesis is that post-training open source creates a path toward more performant, cost-effective and interpretable agent systems, as open-weight models can be hosted within a firm's own secure infrastructure and trained on a company’s own workflows.

4. Real-Time Knowledge (Retrieval & Search)

The core infra enterprise AI tools need to use the web.

Parallel — Powerful API for deep research, data retrieval, and querying the web like a structured database — built for agents that need to reason over live, structured external data at inference time. Founded by former Twitter CEO Parag Agrawal.

TinyFish — End-to-end platform for autonomous AI agents, providing fast full-stack search capabilities so agents can retrieve and act on current information without leaving the inference loop.

Exa — Neural search at web scale, purpose-built for LLMs rather than human searchers. Search API built for agents. Backed by a16z.

Firecrawl — Web crawling and scraping infrastructure for teams that need to pipe fresh external data into AI workflows continuously.

5. Domain Model Builders

The Cursors and Harveys pioneering the playbook.

Cursor (Composer) — Post-trained Kimi K2.5 into Composer, spending 85% of total compute on post-training and RL rather than pretraining. Composer 2.5 matches Claude Opus 4.7 on coding benchmarks at one-tenth the cost.

Harvey — Post-trained a 27B open-weight model against its proprietary Legal Agent Benchmark (1,200+ tasks, 24 practice areas, all-pass grading), working with Baseten Research. Landed inside the closed-source frontier band at a fraction of frontier cost.

Ramp — One of the first enterprise companies to run an own-vs-rent playbook at scale, applying custom post-trained models to expense categorization, financial document analysis, and workflow automation.

Genspark — RFT-trained a Kimi K2 variant that beat SOTA on quality and tool-calling accuracy: +12% quality at roughly half the inference cost of the closed-model baseline it replaced.

Vercel (v0) — RFT-trained an auto-fixer for AI-generated code, hitting a 93%+ error-free rate at roughly 40x the speed of the general-purpose model it used to lean on.

6. Open-Source Foundation Models

The starting points for post-training.

Kimi K2.5 — Moonshot AI’s one-trillion-parameter mixture-of-experts model (~32B active parameters per inference pass). Cursor’s foundation of choice; strong on coding.

Qwen 3.5 — Exceptional reasoning, 1M-token context window.

DeepSeek V3.2 — Near-frontier performance on most benchmarks.

Llama 4 — Broadest commercial ecosystem and licensing familiarity.

Why This Matters

The landscape above isn’t your typical squishy 10-year VC projection. This is a live report from what is happening right now in the field.

These companies exist today and are scaling at unheard of growth rates. Surge AI crossed a $3B run rate without raising a single dollar from VCs. Baseten grew its valuation 3x in only five months. Fleet went from launch to $100M ARR in a matter of months. Mercor is circling a $20B valuation as we speak. And that’s just the tip of the iceberg. The infra to post-train, run, and own custom AI models is readily available to any enterprise that is ready to use it. That simply wasn’t the case even 18 months ago.

What’s left is deciding whether you’re ready to jump. Companies like Cursor, Harvey, Rogo and Ramp are all in and now operate models that are better and cheaper than off-the-shelf alternatives. Importantly, these companies have proven that you can build these competitive advantages while still being happy frontier AI lab customers. Their Claude bills are just significantly lower than they would be otherwise.

The infrastructure is ready. The only question is: are you ready to close your Claude terminal and enter the arena?

Next time (The State of AI Adoption in the Enterprise - Q2 Review): Back by popular demand! A follow up to our Q1 2026 Report: Do 95% of enterprise AI pilots really fail? See below for my Q1 Report on Enterprise AI adoption.

![The State of AI Adoption in the Enterprise [Q1 2026 Review]](https://substackcdn.com/image/fetch/$s_!NQj1!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Faae4b440-12e2-4916-ba93-18c4877d2e92_1600x782.png)

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Views expressed are my own and should be considered as such, and are not the views of NextEra Energy Investments (NEI) or NextEra Energy (NYSE: NEE).