The State of AI Adoption in the Enterprise [Q1 2026 Review]

Do 95% of enterprise AI pilots really fail? Making sense of the oft-cited MIT study that seems to pop up in every pitch deck - and what the data actually says.

We’re back with another edition of Scaling the Enterprise. This quarter, we’re launching something new: a recurring quarterly snapshot of how the Fortune 500 is actually deploying AI — not just how they’re talking about it on earnings calls. Buckle up.

TLDR: **Enterprises are better at adopting AI than you think**

📰 The Headline: MIT says 95% of enterprise AI pilots fail. The stat ran like wildfire. The truth is more interesting.

👑 The AI Elite: 92% of the C-suite are cultivating a new class of AI super-users — while 60% plan layoffs for non-adopters.

💰 The Money: Average enterprise AI spend hit ~$7M in 2025 — and is projected to jump 65% to $11.6M in 2026.

🏆 The Agent Milestone: 80%+ of Fortune 500 now run AI agents in production.

🤖 The Paradox: 97% of executives say they’re benefiting from AI. Only 29% see significant organizational ROI.

Part I: About That MIT Report…

You’ve seen the headline: “95% of enterprise AI pilots fail.”

LinkedIn. Board decks. Twitter posts. Earnings calls. Forbes articles. Conference panels. It went everywhere.

The stat comes from MIT’s NANDA initiative — The GenAI Divide: State of AI in Business 2025 — based on 150 executive interviews, 350 employee surveys, and 300 public AI deployments. The finding: only 5% of AI pilots achieved rapid revenue acceleration. The vast majority delivered “little to no measurable impact on P&L.”

This data was real. However, the media narrative was not. Here’s where it went sideways.

What the stat actually measures

The 95% figure measures one thing: whether an AI pilot produced rapid P&L impact within six months. Not productivity. Not cost savings. Not efficiency gains. And it mostly measured pilots in sales and marketing — the lowest-ROI area in the study.

Measured that way, most projects will “fail.” A new hire doesn’t move the P&L in six months either... they often take six months or more to ramp up!

The study’s most important finding got buried: vendor-led deployments succeed 67% of the time. Internal builds succeed one-third of the time. This was always a story about strategy, not technology. This is a better takeaway for enterprises to focus on.

Do 95% of pilots really fail? The counter-evidence:

The data from Q1 2026 paints a more optimistic picture:

72% of enterprises have at least one AI workload in production — up from 55% in 2024 and 20% in 2020.

Organizations deploying AI across core operations report 20–40% productivity gains in year one

Firms moving AI to production average 1.7x ROI; top performers see 10–18x

AI super-users report 5x productivity gains and save nine hours per week

66% of organizations are already reporting real efficiency gains (Deloitte, 2026)

The MIT Report headline should’ve been: “AI works great once you have a plan to demonstrate ROI and start embedding it into actual workflows.” But that doesn’t fit nicely in a tweet. So here we are.

Part II: Where AI Is Actually Working

The enterprises seeing returns aren’t chasing flashy deployments. They’re doing something less glamorous: embedding AI into high-specificity, high-integration workflows that rarely make headlines. The highest-ROI deployments share three traits: domain specificity, deep workflow integration, and buy vs. build.

2A: The Top Use Cases

✅ Where It’s Working: The Winners’ Playbook

Software Development is the clearest success story. AI coding tools have moved from experimental to “how does anyone write code without this?” Engineering teams are cutting PR review time by a third and boosting code throughput by 30-100%. Anthropic has emerged as the clearleader here.

Back-Office Automation produces the highest returns in the MIT study despite getting the least board attention. Case studies show $2–10M in annual savings from replacing outsourced document review and support. Cost savings of 26–31% across supply chain, finance, and operations. The less glamorous and more manual the function, the higher the return.

Healthcare & Clinical Documentation — AI is now demonstrably improving accuracy and efficiency in clinical documentation. Microsoft’s Dragon Copilot documented 17 million patient encounters in Q1, up nearly 5x year over year. The Permanente Medical Group (TPMG) recently published analysis finding that Gen-AI scribes saved physicians an estimated 15,791 hours of documentation time — equal to ~1,800 eight-hour workdays — while also improving patient-physician interactions and satisfaction. Real value — yet nobody’s writing X posts about it.

After 2.5 M uses in one year, TPMG’s ambient AI scribes were found to ease documentation burden, reduce burnout, and improve communication. Customer Support — 90%+ of enterprises are now testing third-party AI rather than building internally. One public fintech abandoned their internal build mid-development to buy instead. The data is clear: specialized, integrated tools win. Robinhood is one notable exception, successfully launching Robinhood Cortex.

Financial Services - Purpose-built AI tools for finance has been another quiet success story. A few cool examples:

Rogo: AI for Financial Services

Concourse: AI for Corporate Finance Teams

Fraud Detection — AI-powered transaction monitoring has cut false positives by up to 200% at leading financial institutions. It’s no longer a pilot. It’s mission-critical infrastructure. See below for an example:

Variance: AI Agents for Fraud Detection

2B: The Rise of the AI Elite

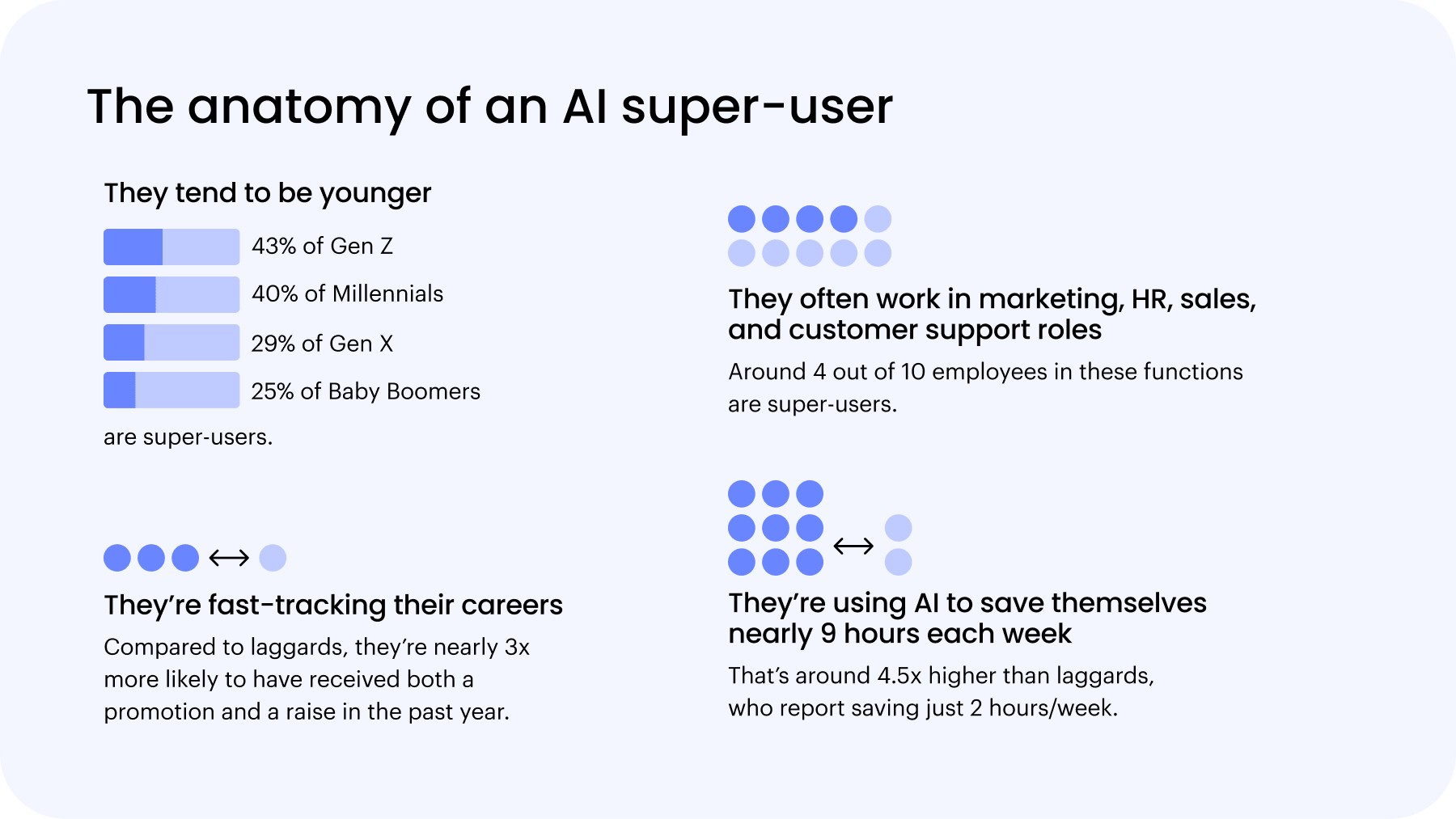

The most underreported story in enterprise AI right now comes from Writer’s 2026 Enterprise AI Adoption Survey (1,200 C-suite executives, 1,200 employees).

The enterprise workforce is splitting in two. Fast.

92% of C-suite execs admit they’re actively cultivating “AI elite” employees, while 60% plan layoffs for non-adopters.

The outcomes gap is stark: AI super-users save nine hours per week — 4.5x more than laggards. They’re 3x more likely to have received both a promotion and a raise in the past year. They’re 5x more productive. The C-suite has noticed.

Who are these super-users?

Skew younger: 43% Gen Z vs. 25% of Baby Boomers

Cluster in marketing, HR, sales, and customer support

Save nearly a full workday every week vs. colleagues who haven’t adopted

77% of executives say employees who refuse to become AI-proficient won’t be considered for promotions. 90% say the rise of AI super-users will require completely rethinking performance evaluation.

Your relationship with AI in 2026 isn’t just a productivity preference. It’s a career decision. Choose wisely.

Part III: What’s Actually Failing — And Why

Now for the honest section. Because AI is also genuinely failing in predictable, avoidable ways — and it’s worth exploring exploring what’s going wrong.

Reason #1: The pilot graveyard

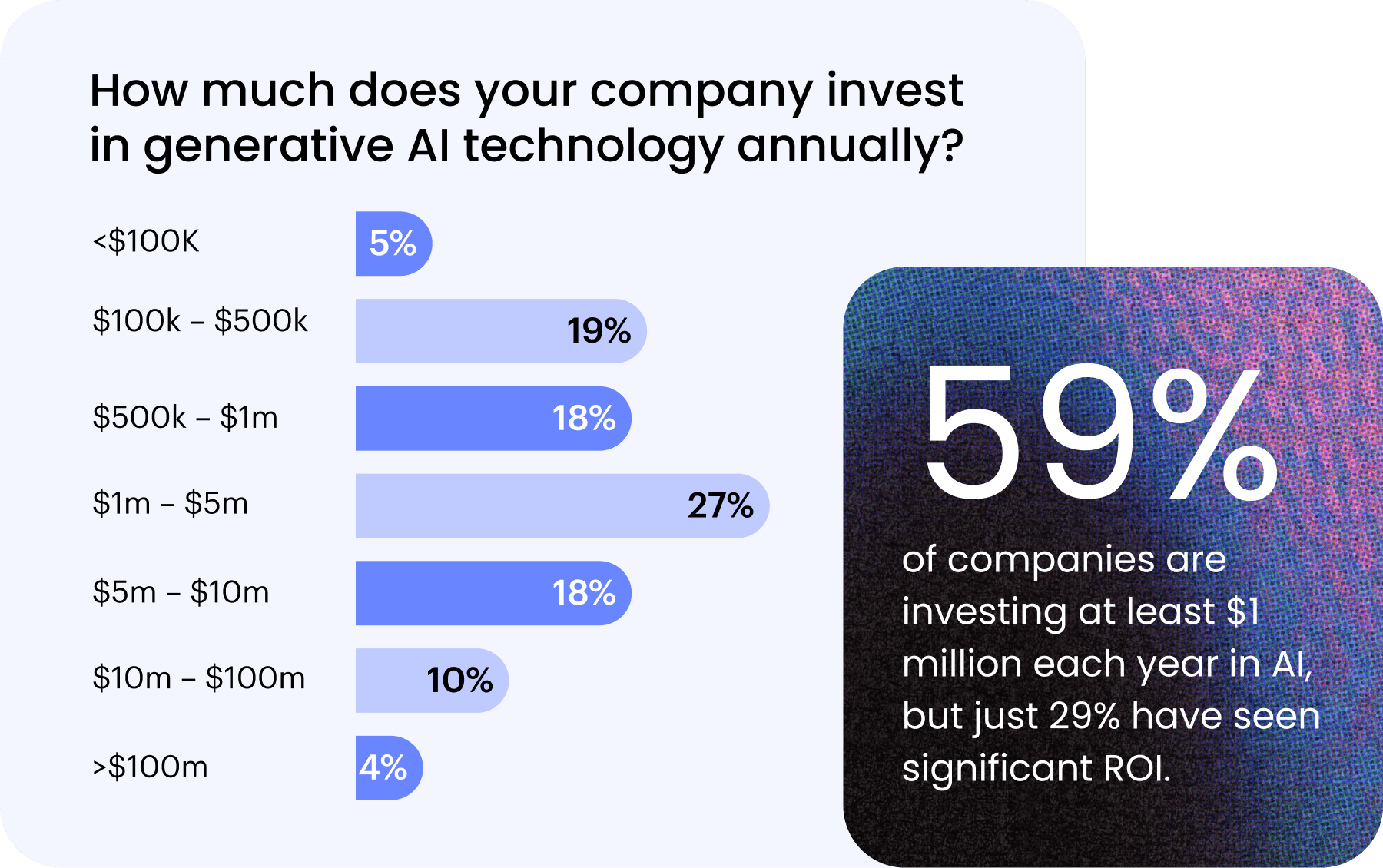

59% of companies invest over $1M annually in AI. Only 29% see significant ROI from generative AI. Only 23% from AI agents. The math is not working.

42% of companies abandoned most AI initiatives last year — up from 17% the year before. The average org scrapped 46% of POCs before production. Not a technology problem. An organizational problem wearing a technology costume.

The top barriers from enterprise CIOs: technical complexity and integration (26%), security and privacy (26%), uncertain ROI (24%). But underneath all three is one root cause: organizations are trying to solve a transformation problem with a highly limited “technology’ budget.

Reason #2: The build-vs-buy trap

Gartner research shows organizations buying existing AI solutions can deploy 60% faster than those building from scratch. And as we covered earlier, our friends at MIT found that vendor-led AI projects had a 67% average success rate (!!).

In our sample, external partnerships with learning-capable, customized tools reached deployment ~67% of the time, compared to ~33% for internally built tools. ~ MIT NANDA

Is the Buy vs. Build debate over for good?

Almost everywhere MIT researchers went, enterprises were building their own tools. And almost everywhere, it was the wrong call. Vendor-led deployments succeed at 2x the rate of internal builds. A specialized vendor has solved the integration and governance problems a hundred times. Your internal team is solving them for the first time, while fighting seventeen other priorities.

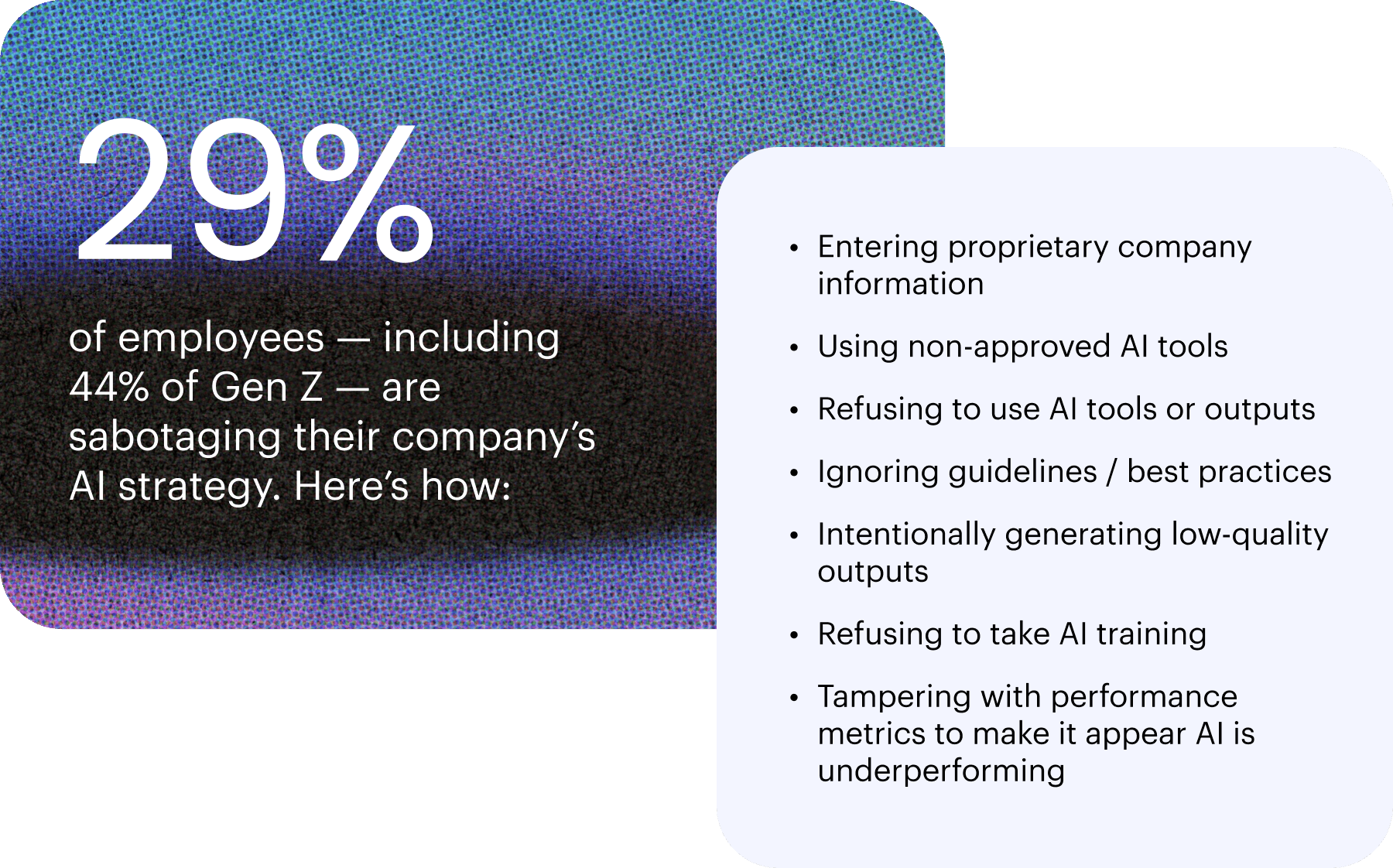

Reason #3: Employees are actively pushing back

Here’s the data point that should be in every CIO’s deck right now. 29% of employees admit to sabotaging their company’s AI strategy — jumping to 44% among Gen Z. How? Entering proprietary data into public tools, using non-approved software, intentionally generating low-quality outputs, refusing AI training, and tampering with performance metrics to make AI look bad.

76% of executives say employee sabotage poses a serious threat. And yet 75% of those same executives admit their AI strategy is “more for show” than actual guidance.

The sabotage is rational. When executives impose mandates without genuine strategy, resistance is the logical response.

Part IV: The Leaderboard — Who’s Winning Enterprise AI Right Now?

The enterprise AI battleground is heating up.

A16z’s Q1 2026 CIO survey of 100 Global 2000 companies is the best public dataset we have. Here’s what it shows.

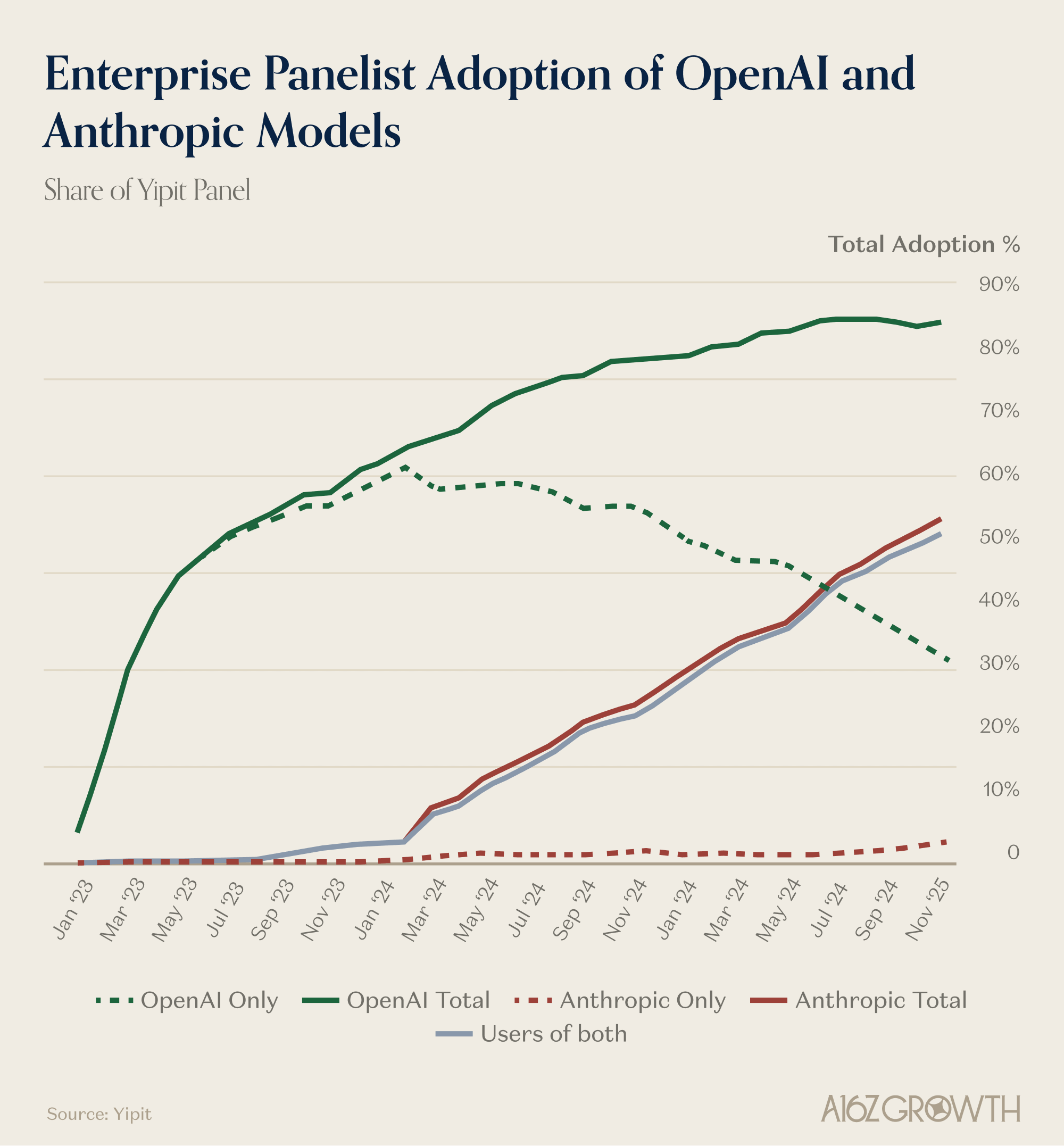

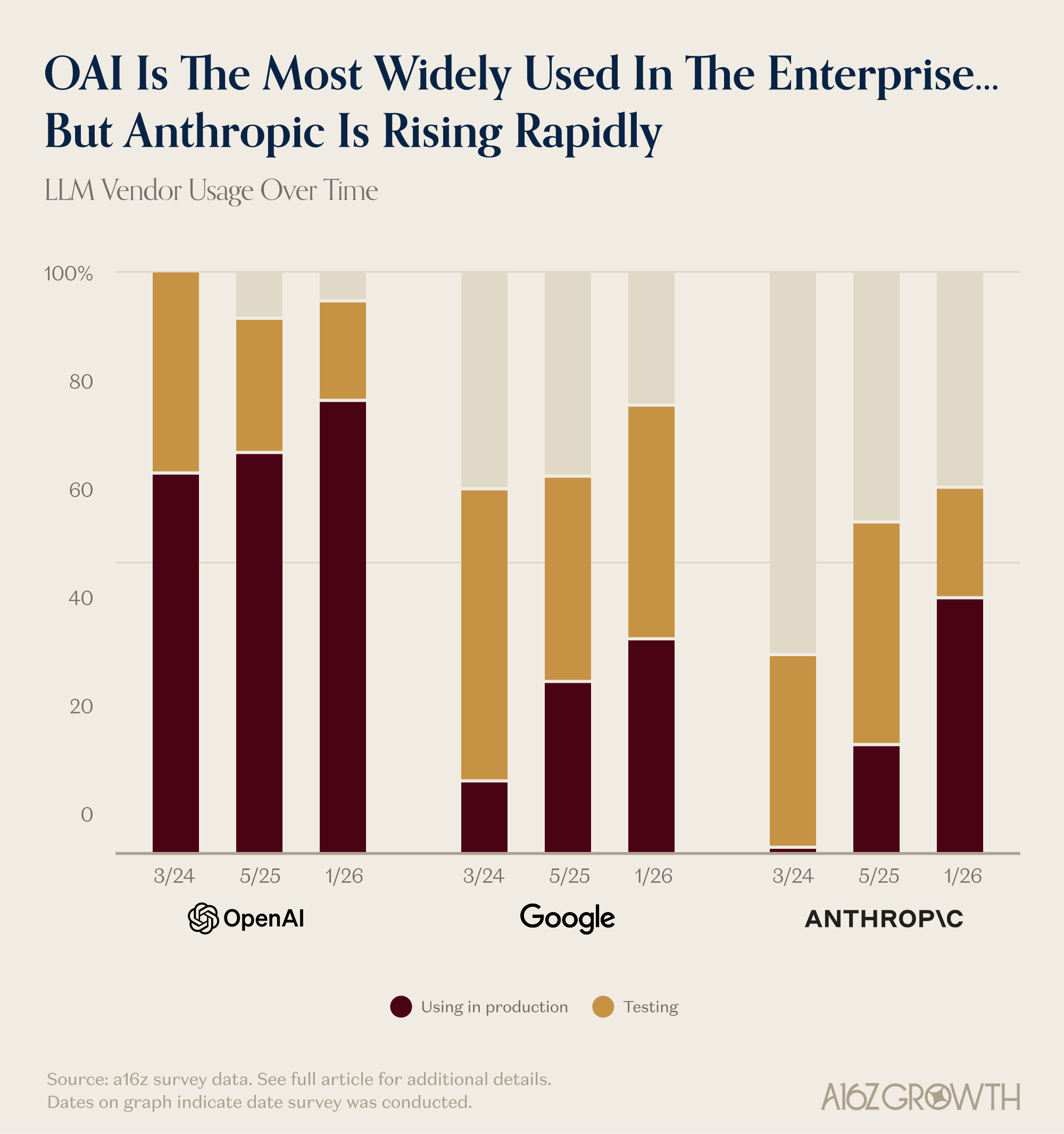

OpenAI is the enterprise leader today, but the tide is shifting…

78% of Global 2000 CIOs use OpenAI in production. It dominated the first wave — chatbots, knowledge management, customer support — and those beachheads are sticky. Switching costs are real — but not insurmountable.

But momentum is shifting. Anthropic and Google have made meaningful share gains with Anthropic’s rise particularly striking, even excluding AI coding startups.

Wallet share tells a similar story. OAI still commands a majority at ~56%, but Anthropic and Gemini are steadily gaining at OpenAI’s expense. The survey also suggests that respondents expect that shift to continue into 2026.

Multi-Model is New Default: The chart below tells the full story. OpenAI’s “only” share has been declining since mid-2024. The total adoption line is holding because customers are also now using both Open AI and Anthropic. The multi-model approach is now the default enterprise.

Anthropic: The story of Q1

Since May 2025, Anthropic posted the largest share gain of any frontier lab — up 25% in enterprise penetration. 44% of enterprises use Claude in production, rising to 63% including testing. Gains are concentrated in software development and data analysis. Critically, 75% of Anthropic customers are already running the latest models — vs. OpenAI, where many enterprises are still on earlier models that “work well enough.”

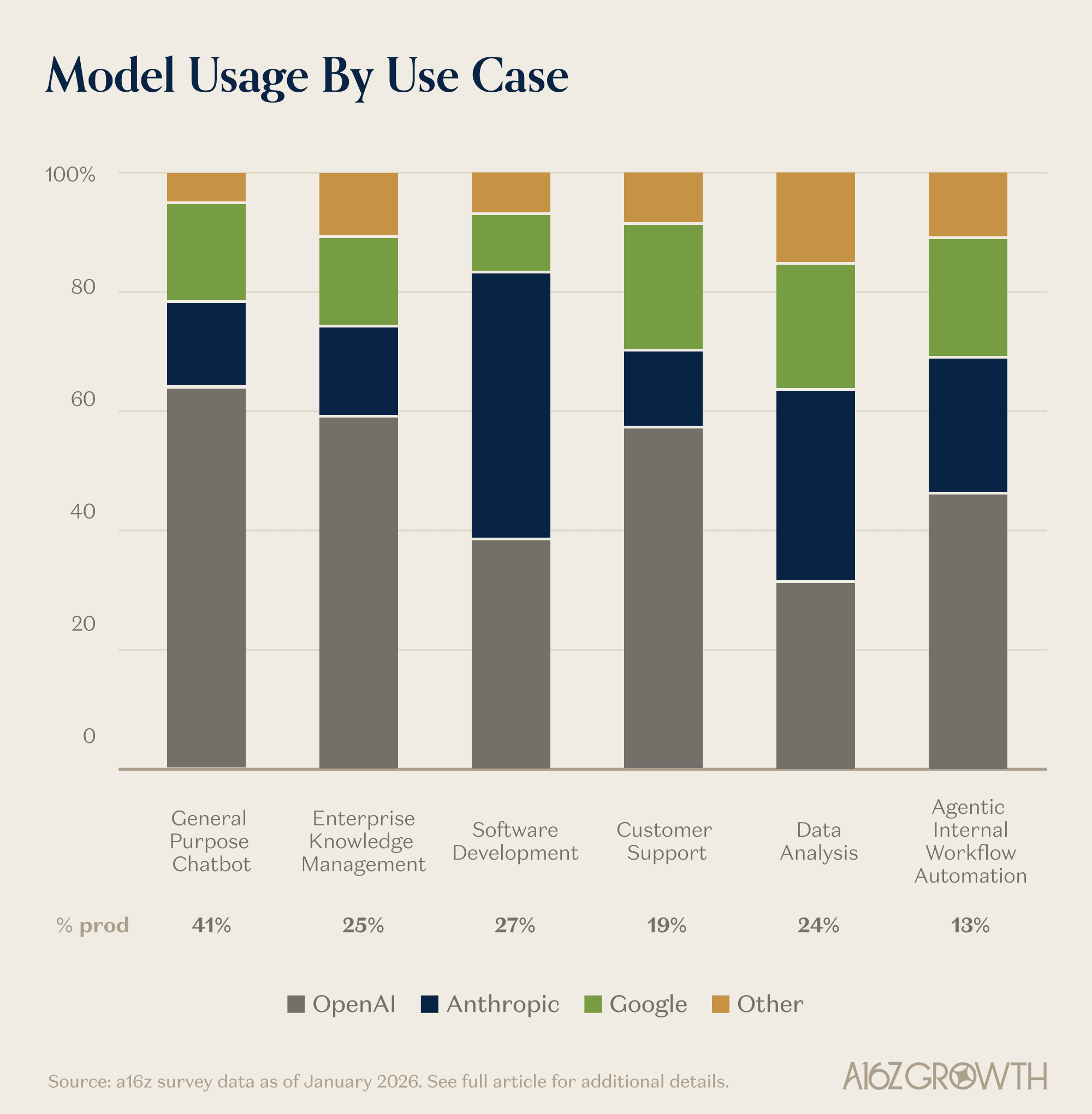

Use case by vendor

The model race is several parallel races:

OpenAI dominates chatbots, knowledge management, and customer support — the early horizontal use cases

Anthropic leads software development and data analysis, where the capability gap is widest

Google Gemini is competitive across most use cases — except coding, where its share lags

81% of enterprises now run 3+ model families, up from 68% a year ago. Nobody is betting on a single horse.

And the actual winner is… Microsoft

While everyone debates Claude vs. GPT-5, the actual enterprise AI winner is a productivity suite from 1989. 90%+ of Fortune 500 companies use Microsoft 365 Copilot in daily workflows. GitHub Copilot has 26 million users. 65% of enterprises prefer incumbent solutions — citing trust, integration, and procurement simplicity.

The incumbent has a 30-year head start and a line item in every enterprise budget. Don’t underestimate that. But the more interesting question is - will adoption stick after a few renewal cycles?

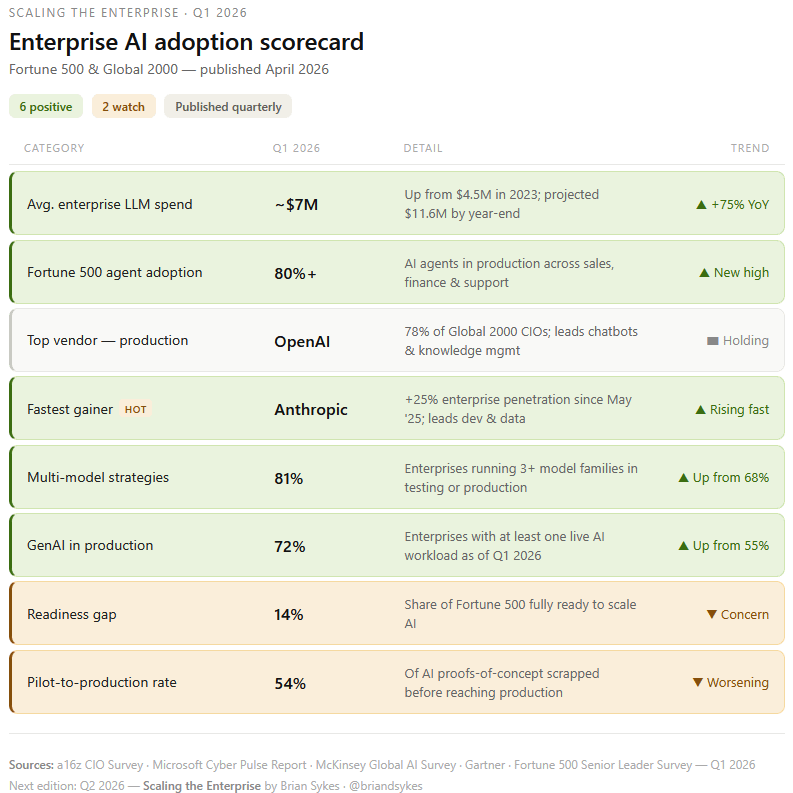

Part V: Q1 2026 Scorecard

One of the persistent problems with enterprise AI coverage is that the data is scattered across a dozen surveys, each with their own methodology and agenda. Starting this quarter, I'm going to be consolidating all of these signals into a single, consistent scorecard — updated every quarter, same format, clean comparisons. The goal is to present a clean view of how Enterprise AI Adoption changes over time.

Here's what Q1 2026 looks like.

Same format, every quarter. Bookmark it.

Final Thoughts: What to Watch in Q2

The 95% stat became a media darling because it confirmed what skeptics wanted to believe. The actual story is more interesting. AI is working — in back-office automation, software development, fraud detection, and clinical workflows. It’s failing where someone bolted a chatbot onto a workflow and called it a strategy. And it’s failing because organizations haven’t figured out how to turn individual productivity wins into enterprise-wide transformation.

Three things I’m watching in Q2:

Can anything stop Anthropic’s current momentum? The a16z adoption chart is clear. If Anthropic’s trajectory holds through Q2, we’re looking at a genuine leadership change by year-end. Switching costs are high — but not infinite.

Build vs. buy debate trending towards “buy”. Vendor-led deployments outperform internal builds 2:1. Enterprises still dedicating engineering resources to LLM wrappers are heading for a painful Q3 reckoning. The emerging category of companies combining model access, governance, and workflow integration in one platform will be the biggest M&A targets of 2026.

Revenue accountability becomes the new mandate. If it continues that only 29% of executives see meaningful ROI from AI initiatives…Boards and activist investors will start asking hard questions. The 29% camp share four traits: AI tied to revenue outcomes, governance built before scaling, business teams owning AI workflows, and the whole thing treated as Org redesign.

AI spend is no longer an innovation budget. It's the cost of staying alive. The companies still treating it like an experiment aren't being cautious — they're falling behind. Q2 will separate the winners from the losers. More soon.

Disclaimer: The information contained in this article is not investment advice and should not be used as such. Investors should do their own due diligence before investing in any securities discussed in this article. This article is based on my opinions and should be considered as such, not a point of fact. Views expressed are my own and are not the views of NextEra Energy Investments (NEI) or NextEra Energy (NEE: NYSE).